Taxes are a stressful topic for most, but to make tax time a little easier this year check out the top three mistakes made on tax returns- and how you can avoid them!Taxes.

Did you wrinkle your nose at that word? Get a shiver down your spine? For most people, taxes are a serious pain point in their adult lives. For the sake of life-long learning, and expanding the advice available on Friend of Finance, I’m currently enrolled in an Income Tax Course, and one-third of the way to becoming an Enrolled Agent (a tax advisor who is allowed to represent people on tax matters before the IRS). What does that mean? That I’m learning a heck of a lot about taxes. And unlike other areas I’ve studied (cough, insurance, cough) the more I learn about taxes, the better I feel. Our system in the U.S can be frustrating at times, but these weird, tricky little math rules that taxes are, are actually set up to help us in a lot of ways, not to try and hurt us. How our tax money is used is a completely different topic that I’m not getting into, but the system behind the Internal Revenue Service collecting our money is constantly evolving because people are trying to improve it. There are a TON of rules when it comes to taxes. But, a lot of these rules are there to protect taxpayers, give credits and deductions to people who need them, and try to make our system as efficient as possible. With that being said, it’s easy to make mistakes and get stressed come tax time. In my last class, I asked my instructor what her top 3 mistakes she saw in her years of experience preparing returns, and to be honest, I was a little surprised with her answers!

0 Comments

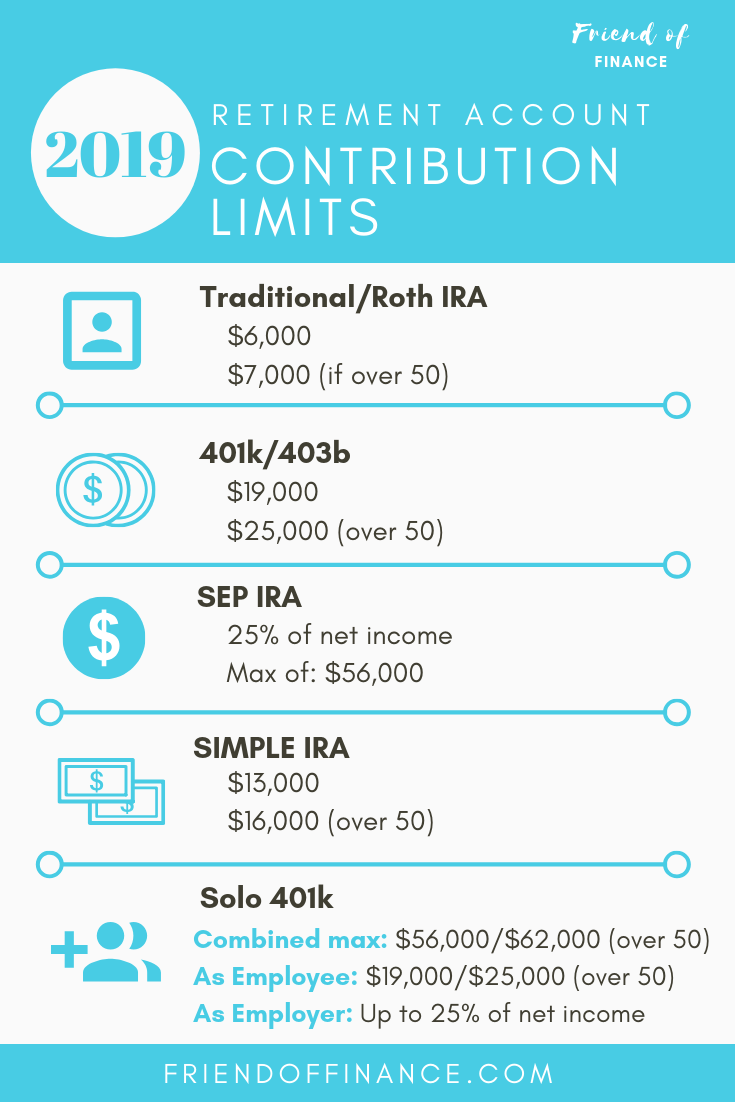

What are the retirement account contributions for 2019, and how can maxing out your retirement accounts help you long-term?Saving for retirement is important, and more people are becoming aware of the importance with the growing FIRE movement (Financial Independence, Retire Early). One of the key ingredients to a successful retirement, especially if you plan on retiring early, is maxing out your retirement accounts. If your plan is to retire early, it’s important to note that early withdrawals (money taken out before you are age 59 ½) from the qualified retirement accounts listed below could be subject to a 10% penalty. For this reason, saving and investing in regular brokerage accounts or taxable accounts is also recommended.

Every so often the IRS will announce adjustments to cost of living expenses, which will increase the contribution to retirement accounts and pension plans. 2019 was a year that saw an increase for contribution limits, for the first time since 2013. This increase means you can put more away compared to previous years. Keeping on top of the limit increases is important for anyone actively trying to max out their retirement accounts, or for those who are doing future planning forecasts prior to retirement. The longer you have before retirement, the more these increases are actually worth because of time and compounding interest. I’ll show you what I mean after we go over the new increases.  Investing is a great tool for building wealth, but there are some financial milestones you should consider before you start investing.Investing has a stigma for being complicated, or something that is only for people that have a lot of money. While there is a learning curve when you first start investing, it’s important to know that anyone can invest, and you don’t need a huge sum of money to begin.

1. Have an emergency fund. The money you plan on investing should be money you are comfortable not touching for a long period of time. It is not an extension of your checking or savings account, and ideally shouldn’t be taken out until you’ve hit the goal or time that money was designated for. So before you invest your money, make sure you have an adequate emergency fund to reduce the need to dip into your investments. An emergency fund should have 3-6 months of living expenses set aside.  Making the switch to a high-yield savings account is one of the easiest ways to grow your savings. Not only can you earn a higher interest rate, but you can better protect your future purchasing power too.A few years ago, I never put much thought into my savings account. I thought simply having one, and one that had some money in it, was a financially responsible move.

In fact, before I went on my year-long trip backpacking around Australia, the only consideration I gave my savings account was to have enough for 15 months of student loan payments to be auto-deducted. All I worried about was having enough for those payments, I wasn't concerned about the interest that was being earned, or the service fees being charged.  The learning curve of investing may seem overwhelming, but it doesn't have to be. Learn about the three things that can make you a more confident investor!Investing. It can be an intimidating word if you aren't doing it. But, if you are, and if you understand your investment process, that intimidating feeling shifts to empowerment.

If you are currently intimidated, here are the three things you should know before you start investing.

Thanks to social media keeping track of our past activities, I was recently reminded that this summer marks the 5th anniversary of getting my bachelor's degree. I would love to tell you that all of my student loans are paid off, but I'm not quite there yet. Instead, I will share the 5 things that I have learned about student loans since graduating.

An employer plan like a 401k or 403b is the most common way to save for retirement. But what if you aren't offered a retirement plan through your work?Planning for retirement is one of those things that we tend to leave for an older version of ourselves... but the effects of starting young can have an amazing result for producing extra digits in your retirement account! So, regardless of age, getting clued in on how you should be saving for retirement is important, and you can learn more in this free course.

The most common way to save for retirement is through an employer sponsored plan, like a 401k or a 403b. For many, this is their sole source of retirement savings. But what happens if you don’t have access to a 401k or 403b? According to 2018 research by Congressional Research Service, only 64% of workers in the U.S have access to a Defined Contribution Plan (401k, 403b or 457b) and of that, only 47% are participating. Does this mean the majority of Americans are not saving anything for retirement?  These three financial components are crucial to starting your business and taking advantage of perks like self-employed retirement accounts.Thanks to the internet, it is now easier than ever to start your own business. A few google searches will tell you everything you need to know to get your business up and running. There are an abundance of free, online courses to guide you through specific topics, and social media has created an affordable place to market your business to your target audience. We often hear about the perks of being self-employed, “Oh, the freedom, the creativity, setting your own hours, pursuing your dream!” Yes, those are all great things, but what about the less glamorous aspects of running a business?

Not having access to a retirement plan can be detrimental to your future, it's important to know your alternatives to an employer 401k when you're self-employed.Being self-employed certainly has it’s perks, but making the trade-off of working for an employer versus working for yourself comes with quite the learning curve, especially when it comes to retirement savings.

The most common method of saving for retirement for Americans is through an employer defined contribution plan, like a 401k or 403b. These accounts are great, because not only do they come with a heap of tax benefits, your employer is the one setting it up for you, and often they are matching up to a certain percentage of your contributions. Who doesn’t like free money?! When you are self-employed, it’s a whole different story, because the only one responsible for your retirement savings, is you. Luckily, you have several options out there. Read on to find out what accounts you can take advantage of, or check out this free online course that will walk you through all of your options, and tell you how to get started.  Summer spending can be hard on our wallets, but these five tips will help make sure you're not going into debt for your fun.The sun is out, your friends have emerged from hibernating, the potential things out there that you can spend your time (and all your hard-earned cash) on have increased tenfold! For all those that have survived another gloomy winter, the presence of good weather feels so good. So good, that you don't even care that you're eating out more, splurging on drinks, buying those cute new summer clothes, planning trips... until you check your bank balance and credit card statements.

Read on for 5 tricks to save yourself from going in the red this summer, and make sure you read to the end- I may be biased but #5 could be the most important! |

Archives

April 2021

Categories |

RSS Feed

RSS Feed