Are you hearing a lot of what you "should" be doing with the current market climate, but actually have no idea of how you even start investing? Look no further for a simplified breakdown of how to open your first investment account.

The 5 Steps to Start Investing

If you’re reading this, chances are you are feeling slightly overwhelmed about your current, nonexistent investment portfolio. The fancy financial verbiage probably makes you want to cover your ears and carry on with life, not worrying about the state of your future retirement years. I get it, I’ve been there. Up until age 25, I thought I had plenty of time before thinking about retirement. Surely I don’t have to start thinking about that until I’m 50 or so. I knew I should be saving and chipping away at my student loans, but retirement?! Not even on my radar. That is, until I got a job in the financial industry, and was face-to-face with its importance on a daily basis. I quickly learned that retirement isn’t something you should wait to save for, in fact, the opposite is true. The earlier you start investing for your future, the easier it is to become a millionaire. Or a multi-millionaire. But then running the numbers of waiting until you’re older and in your 40’s and 50’s? You’ll need to put a LOT more money away to reach a million. Okay, you get it- it’s important. BUT HOW DO YOU START?! No need to yell! I’ll show you right now, in 5, easy steps. 1. Decide what kind of of investment account to open

The type of account you open will vary based on your goal.

If you are investing for retirement, you’ll want to use an account that has retirement tax benefits, like a Traditional IRA or a Roth IRA. If your employer offers a 401k or 403b at work, these will also have tax benefits and are designated solely for retirement. Only employers can open 403b’s/401k’s, but you as an individual can open any of the following retirement accounts: Traditional IRA Roth IRA SEP IRA (if you’re self-employed) Currently the rule with IRA's is you can't pull money out before age 59.5 without paying a 10% penalty. There are some loopholes and exceptions, especially if using a Roth IRA, but as a rule of thumb- leave your IRA's alone until retirement. Now, you might be thinking you’re too young to start saving for retirement, or that it isn’t necessary yet… get this idea out of your head! The sooner you start saving for retirement, the more time you have to take advantage of compounding interest! If you want to invest in something outside of retirement accounts, and access that money before age 59.5, you would open a brokerage account. This can be an individual account or a joint account. It doesn’t have the sweet tax perks of retirement accounts, but it also doesn’t have the limitation of when you can pull your money out without penalty. A brokerage account should be used if you plan on taking the money out before your retirement years. 2. Know where to open your investment account

Investment accounts aren’t in the same category as your standard checking and savings, and they are housed by what is called a ‘custodian’. You might be familiar with some of the big ones like TD Ameritrade, Fidelity, Vanguard and Charles Schwab, and as we shift to online banking, more and more are opening up.

I personally use TD Ameritrade, and would recommend them, or either Fidelity or Schwab. If you plan on only investing in Vanguard funds, opening an account at Vanguard is a good choice too. They are all reputable companies, and all have recently done away with their trading fees. Yay for free trading! You’re in a lucky time because opening an account online is easier than it has ever been. You’ll need some personal information handy, like your birthday, address and social security number, and you’ll have to be ready to share some simple employment information, but the opening process should take less than 15 minutes. You will either have online access to your new account shortly or, more likely, have to wait a few days for a welcome packet to arrive via snail mail. Your welcome packet will have your account number(s) and instructions for logging in for the first time. 3. How to get money into your new investment account

Once you are in your new investment account, you will be able to connect your checking or savings directly to it, and transfer funds immediately via ACH. There are other ways to transfer money into your account, like writing a check or completing a wire transfer, but ACH is the quickest and cheapest method.

Link your checking or savings that you wish to move money from by providing your account type, routing number, and account number. Save this to your investment account for future transfers! 4. Decide what to invest in

This is where a lot of people unknowingly make a mistake. They assume that because the money is now in their investment account, they are invested… No, no, no.

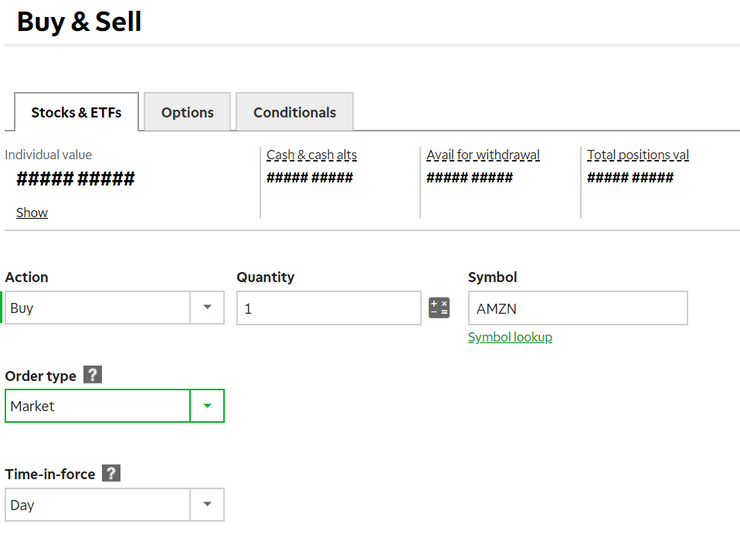

When your cash is moved over, it is just that- cash. If you look closer at your account, you will see something like ‘Available cash balance $XXXX ’. This money is not invested yet, and it’s up to you, the investor, what it is you want to invest in! Do you want to invest in the stocks of your favorite companies, like Amazon, Facebook, and Starbucks? Simply look up their symbol, or ticker, and submit a trade order.

Submitting a ‘market order’ means your trade will be processed at the current going price. Setting a ‘limit order’ allows you to input the price you would like to buy at, and if it reaches that amount, your order will be submitted. You will also be asked for time parameters for how long you wish the limit order to be open. Keep in mind, picking stocks is not for everyone (I would even argue that it isn't for most) and there are other options out there. You might decide to invest in ETFs (exchange-traded funds) or mutual funds, which have a large collection of individual stocks, all inside one fund. Using ETFs or mutual funds can provide a simple and popular investment strategy; indexing. Before making your first purchase, it’s worth doing a bit of research on what exactly you want to invest in. If that overwhelms you, I would nudge you in the direction of a low-cost, total US market ETF from Vanguard… VTI. When you invest in VTI, or other, similar total US market index funds, you are actually buying a small piece of many, many companies, all inside one share (3534 in VTI, to be exact). And being a total market fund- you’ll get a piece of everything. Large companies like Microsoft, Apple, Amazon, Google and Visa, and mid-size and small companies, like Lululemon, Twitter, and 5 Below. Heck, even Build-a-Bear is in there. This is a great way to achieve diversification in your portfolio with just one fund, especially if you are just starting out and can’t afford to buy a variety of individual stocks. 5. AUTOMATE IT!

Congratulations, your account is opened, funded, and you know how to place your first trade, WOOHOO!

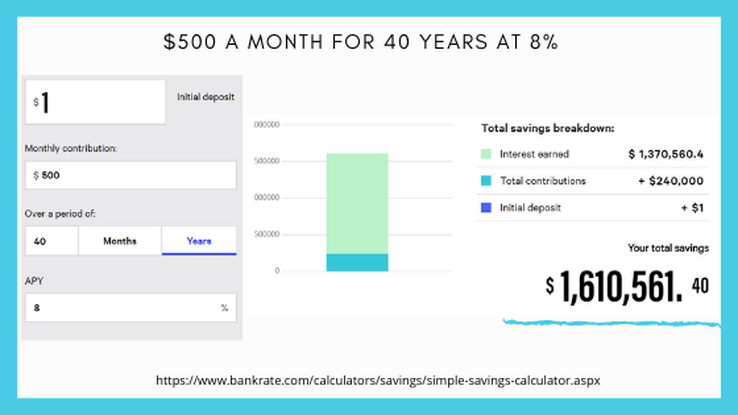

Now, the real secret to growing your wealth… being consistent. The easiest way to defeat human laziness is with automation, and your investment accounts are the perfect place to put automation to work! Decide how much you want to contribute on a regular basis, whether it’s weekly, bi-weekly, monthly or quarterly, and set up an automatic, recurring deposit from the account you linked earlier. I recommend setting up your deposit for the day after you get paid- the sooner it is out of sight, the less it will be missed! Paying yourself FIRST is one of the best things you can do to accumulate wealth, so make sure your new automatic deposit into your investment account gets priority over your mindless spending! If you aren’t sure how much you can put away, it’s important to first know the rules if you are contributing to a retirement account. For Traditional and Roth IRA’s, there is an annual limit of $6,000 for 2019 and 2020. If your goal is to max out your account with the full amount, $500 a month will get you there. And what does $500 a month look like after 40 years, averaging an 8% return? I’m glad you asked…

Over $1.6 million!

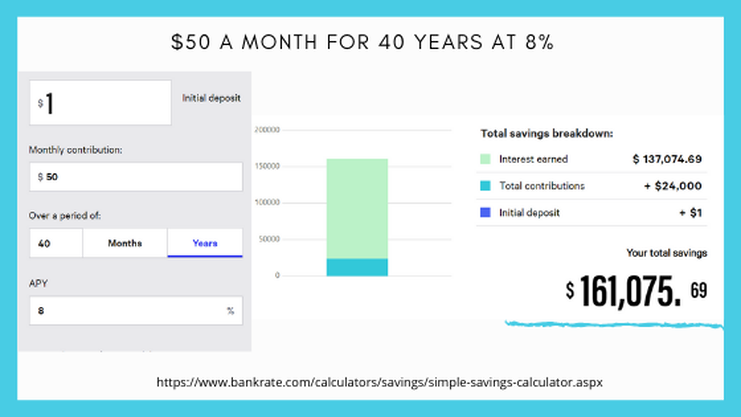

And the best part?! The total contributions were only $240,000 over those 40 years, with over $1.3 million coming from compounding interest. This is why it’s important to start as early as possible! Now, I know a lot of us don’t have an extra $500 a month laying around. If you feel stretched too thin as is, and $500 is way out of your budget, it’s okay to start smaller. If you are brand new to investing and have a lot of other financial goals on your plate, even just starting with $50 a month will make a huge difference over the course of your life. Just $50 a month over the course of 40 years looks like...

While obviously not as impressive as $1.6 million, it is still a substantial amount that again, is mostly made up of compounding interest! In this scenario, only $24,000 is invested over the 40 years, and over $137,000 was made from compounding interest. TAKEAWAYS! Investing is not as complicated as you might have thought! You can open an account online within 15 minutes, and start investing in stocks, ETF’s or mutual funds once your account is opened and funded. It’s never too early to start saving and investing for important, long-term goals, and the earlier you start the more time you will have to take advantage of compounding interest! If you have questions,LET ME KNOW H E R E ! Want to stay in the money loop? Join my community here, where I send out weekly emails that are a mix of helpful and inspirational, with a splash of "get your money shiz together my friend!" Sign up below :)

3 Comments

4/6/2020 01:38:35 pm

Its a tough time for learning to invest but the worst time is learning 20 years from now! Thanks for keeping it easy. Happy health and savings!

Alicia

4/7/2020 06:36:59 am

You are absolutely right! When it comes to investing, the sooner the better! Leave a Reply. |

Archives

April 2021

Categories |

RSS Feed

RSS Feed