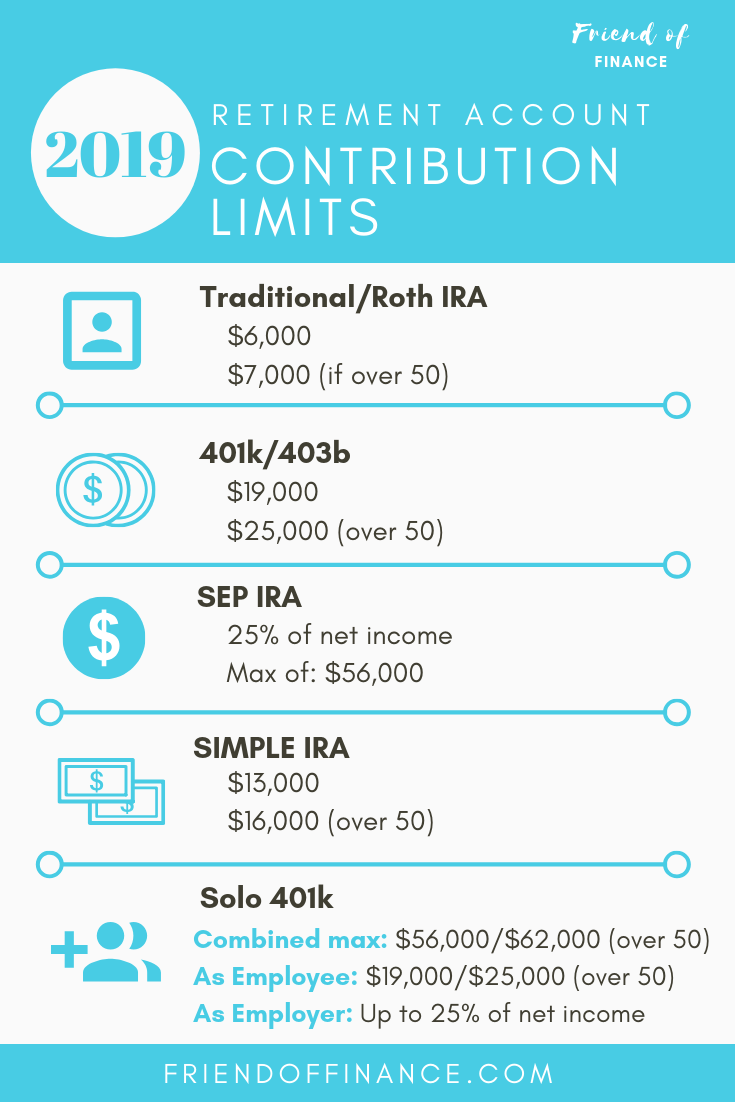

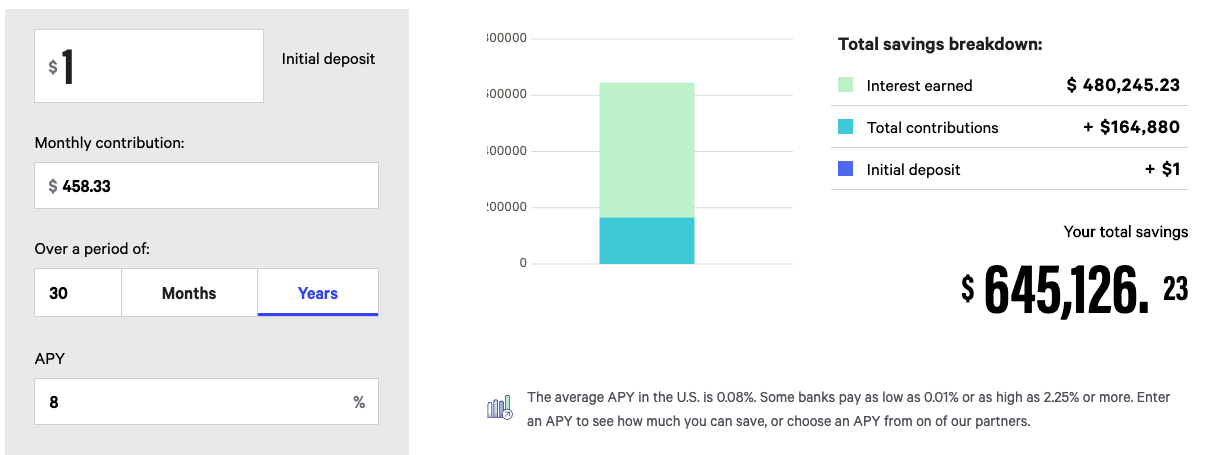

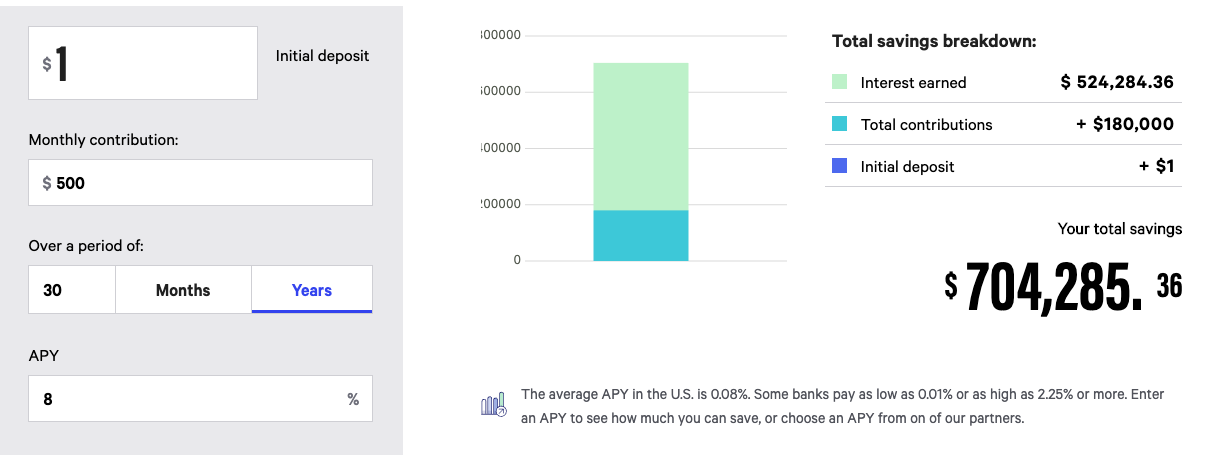

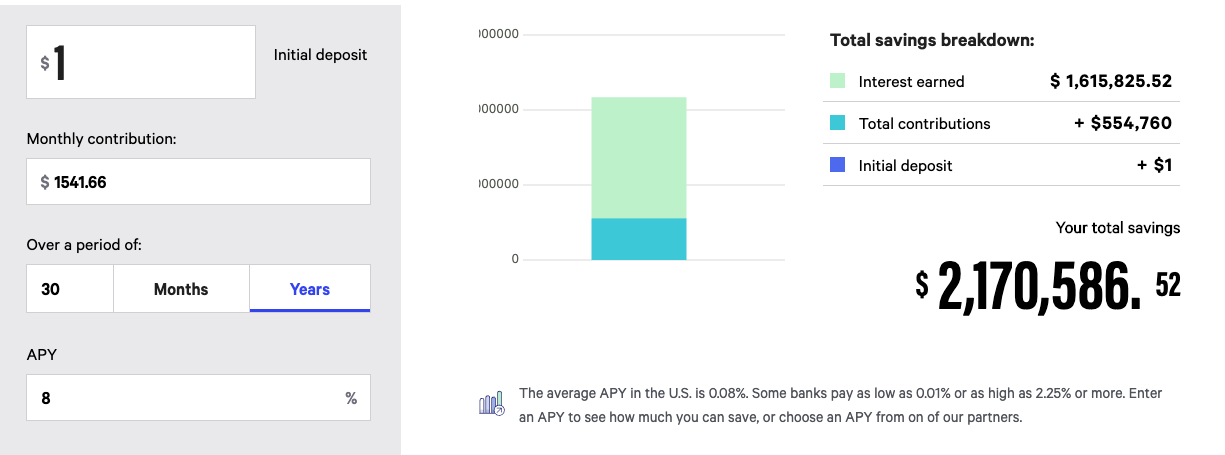

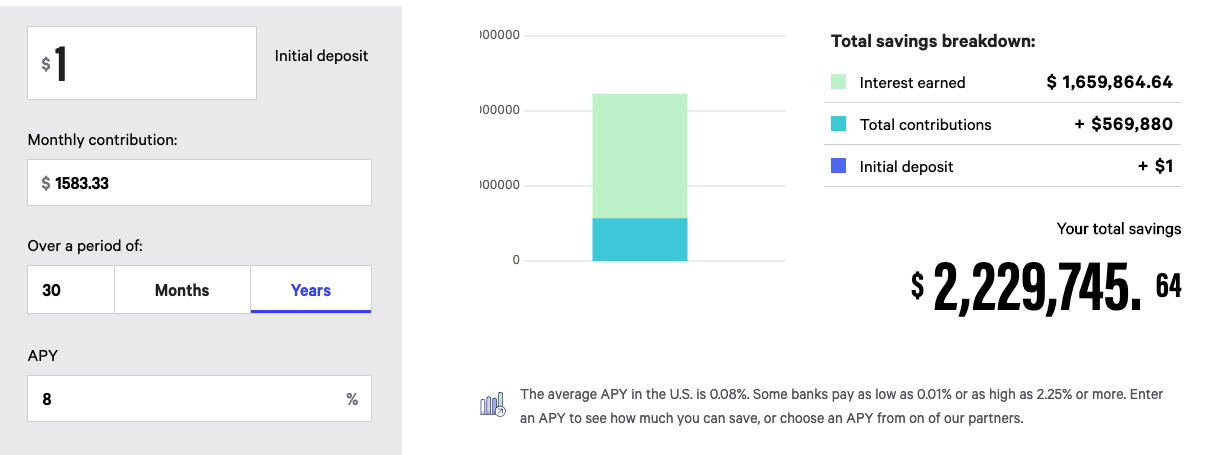

What are the retirement account contributions for 2019, and how can maxing out your retirement accounts help you long-term?Saving for retirement is important, and more people are becoming aware of the importance with the growing FIRE movement (Financial Independence, Retire Early). One of the key ingredients to a successful retirement, especially if you plan on retiring early, is maxing out your retirement accounts. If your plan is to retire early, it’s important to note that early withdrawals (money taken out before you are age 59 ½) from the qualified retirement accounts listed below could be subject to a 10% penalty. For this reason, saving and investing in regular brokerage accounts or taxable accounts is also recommended. Every so often the IRS will announce adjustments to cost of living expenses, which will increase the contribution to retirement accounts and pension plans. 2019 was a year that saw an increase for contribution limits, for the first time since 2013. This increase means you can put more away compared to previous years. Keeping on top of the limit increases is important for anyone actively trying to max out their retirement accounts, or for those who are doing future planning forecasts prior to retirement. The longer you have before retirement, the more these increases are actually worth because of time and compounding interest. I’ll show you what I mean after we go over the new increases. 2019 Contribution Limits for Retirement AccountsHere are the new limits for 2019. Individual Retirement Accounts: Traditional IRA, Roth IRA Old Limit 2018: $5,500 New Limit 2019: $6,000 Catch-up contribution for Individual Retirement Accounts for those aged 50 and over (unchanged) 2018: additional $1,000 2019: additional $1,000 Employer or government sponsored plans: 401(k), 403(b), most 457 plans and Thrift Savings Plans 2018: $18,500 2019: $19,000 Catch-up contribution for employer/government plans for those aged 50 and over (unchanged) 2018: additional $6,000 2019: additional $6,000 Self-employed accounts: SEP IRA, SOLO 401K 2018: $55,000 or 25% of net compensation 2019: $56,000 or 25% of net Compensation SIMPLE IRA 2018: $12,500 2019: $13,000 Catch-up contribution for SIMPLE for those aged 50 and over (unchanged) 2018: additional $3,000 2019: additional $3,000 Are you eligible to max our your accounts?It’s important to note that the ability to max out certain accounts will vary depending on income, tax filing status, and whether you are participating in an employer plan. To see if you fall under any income phase-outs where your contribution may be limited, check out what the IRS says here. Potential returns on your extra contributionsWhile the increase isn’t huge (only a $500-$1000 increase per account), the potential difference it could make in your retirement account is. An extra $500 a year might not seem like much, but when you calculate the potential returns and compounding interest you have to gain on that additional $500 or $1,000, that addition can make a big difference. Before we crunch the numbers, it’s important to understand where your return is coming from, or not coming from. There are a lot of variables in place that determine your overall rate of return, like how aggressive you are invested, i.e. are you in 100% stocks and 0% bonds, or are you more conservative, and have 30-40% of your portfolio in bonds? Typically, a higher allocation to stocks or equities will give you a higher return in exchange for more risk. The returns you can expect will also vary based on the overall economic climate, which is constantly changing. We know there will be good years and bad years, bull markets and bears, but, typically, the longer you have to be invested, the higher your average will be. This is another reason why starting young is so important when it comes to retirement savings. Since inception in 1926, the S&P 500 has averaged an annual return of 10%, but it’s important to remember that past performance does not guarantee future results. It’s also worth noting that the S&P is made up of the 500 largest US companies, so this would not be an accurate benchmark for somebody with a diversified portfolio, or someone who has a percentage allocated to bonds. After understanding what to expect, and knowing it’s not guaranteed, let’s run a comparison of what these contribution increases could actually look like after so many years. In the next examples, we will use an annual return of 8%, and hypothetically max out our retirement accounts with both the previous contribution limit, and the new one. All examples will start with $1 to start. Maxing out your Traditional IRA or Roth IRA at the previous limit- $5500 annually for 30 years ($5500 divided by 12 months = $458.33 per month)  After 30 years, total contributions equals $164,880 Interest earned equals $480,245.23 For a total of $645,126.23 Maxing out your Traditional or Roth IRA with the NEW limit - $6000 annually for 30 years ($6000 divided by 12 months = $500 per month)  After 30 years, total contributions equals $180,000 Interest earned equals $524,284.36 For a total of $704,285.36 Between the previous contribution limit and the new one, there is a difference of $59,159.13, or just over 9%, all from being able to contribute an additional $15,000 over the course of 30 years. Let’s take a look at an account with a higher limit, like a 401k/403b. Maxing out your 401k or 403b at the previous limit- $18,500 annually for 30 years ($18,500 divided by 12 months = $1541.66 per month)  After 30 years, total contributions equals $554,760 Interest earned equals $1,615,825.52 For a total of $2,170,586.52 Maxing out your 401k or 403b at the NEW limit- $19,000 annually for 30 years (19,000 divided by 12 months = $1583.33 per month)  After 30 years, total contributions equals $569,880

Interest earned equals $1,659,864.84 For a total of $2,229,745.64 In this example, we are still only able to add an additional $500 a year, so our total increase is the same as the Traditional/Roth example, for an extra $59,159 after 30 years (2.72% more). Takeaways If your goal is to max out your retirement accounts, be aware of limit increases, because they can have a big impact on your ending balance. The impact is even greater for the accounts with the lower limits (like the Traditional and Roth IRA). In these examples we are assuming these current limits for the next 30 years… based on past increases, it is likely that the IRS will have several contribution increases over this time span. This means potential for growth could actually be much higher, if you are able to increase your contributions along with the limit. If you are just starting on your investing or retirement saving journey, the idea of putting that much money away every year can be daunting. Life is expensive, especially with increased pressures on having a picturesque life on social media. Remember, no matter where you are on your journey to wealth, investing something is better than nothing. The impacts of the $500 increase were actually much greater in the Traditional/ Roth IRA than in the 401k/403b (a 9% increase in ending balance compared to a 2.7%) which helps show that as long as you have time and compounding interest on your side, a little money can go a long way. If you have questions about investing or opening your own investment accounts, feel free to reach out to me here. If the idea of having a lot of money in a few decades is exciting, and something you want to start for yourself, make a plan to start! Friend of Finance now offers an affordable monthly service for investors that are just starting out (or those who haven’t started yet) which covers opening accounts, rollovers, savings strategies and investment management. You can learn more about these services here. Sources: https://www.irs.gov/newsroom/401k-contribution-limit-increases-to-19000-for-2019-ira-limit-increases-to-6000 https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits https://www.investopedia.com/retirement/ira-contribution-limits/

0 Comments

Leave a Reply. |

Archives

April 2021

Categories |

RSS Feed

RSS Feed