It's time to shed some romantic light on those accounts you've been avoiding!

First things first, define sexy...

Sexy saves money, grows money and makes money, and believe it or not, your retirement account is capable of doing all three. Whether or not it will though, is up to you. How do retirement accounts save you money?

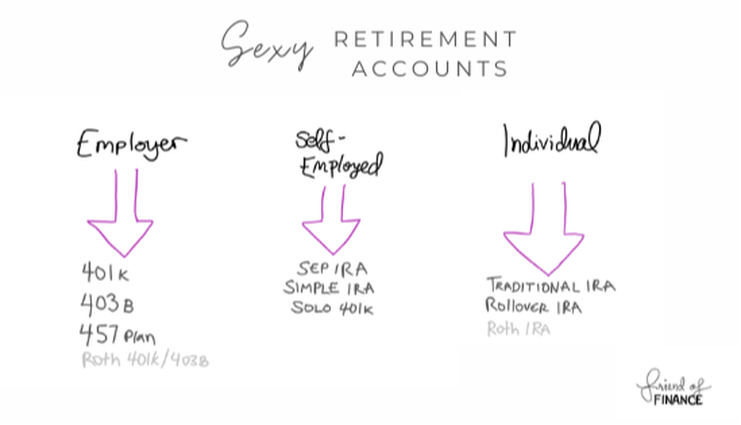

There are a few different types of retirement accounts, and while all of them will help you save money, they work in slightly different ways. Retirement accounts can be broken into groups by who can open them; either an employer or an individual. If you are self-employed, you get a mix of both worlds!

Note: Roth 401k's and Roth IRA's are included in the list of great retirement accounts, but they have different tax rules that I don't dive into with this post. To learn more about the Roth, check out this post next.

It's time to stay up to date on tax savings and retirement account rules, get a free download the Financial Cheat Sheet! This is a MUST HAVE if you're self-employed!.

Employer Plans: 401k's 403b's and 457 Plans

When you are in the working portion of your life, you might run into an employer-sponsored retirement plan, like a 401k, 403b, or 457 plan. This is an account, or “investment vehicle” that is opened by your employer and receives both employer and employee contributions. It is designed for pre-tax contributions, meaning a portion of your paycheck can be diverted into one of these accounts before taxes are taken out.

These employer accounts are extremely helpful for saving, you have none of the headache of establishing the account, and you can easily control the amount you deposit into it. Plus, there are some sweet tax savings. All of the money you put into these accounts gets deducted from your income when you file your taxes, thus lowering your taxable income, in turn, lowering the amount you need to pay in taxes. The more money you make, the more taxes you pay, so lowering your taxable income with retirement contributions can be very helpful, especially if you’re in a high tax bracket. Even if you aren’t making a lot, you will still see some amazing tax benefits.

While you save for the future, you also might be getting an employer match. This means someone else (your employer) is also saving for your future, meaning EVEN MORE SAVINGS! They also get to deduct all of the contributions made come tax time, providing some more tax savings for themselves there.

IRA’s: Traditional, Rollover, SEP, SIMPLE

These retirement accounts are opened on an individual basis, not through an employer. If you are self-employed, you also have the option of opening a SEP IRA or a SIMPLE IRA. When you put money into one of these accounts, you are following the same principle as in the employer-sponsored plans above- by saving and investing for your future, but this time you will not be regulated to the investment options within your 401k. In your IRA, you are free to buy or trade whatever you want.

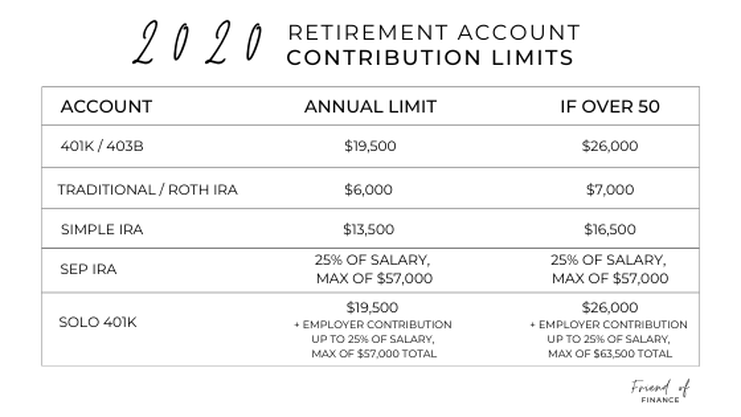

There are annual limits on these accounts, and they are all different. It’s important to be aware of what the limits are, and make it a goal to max them out!

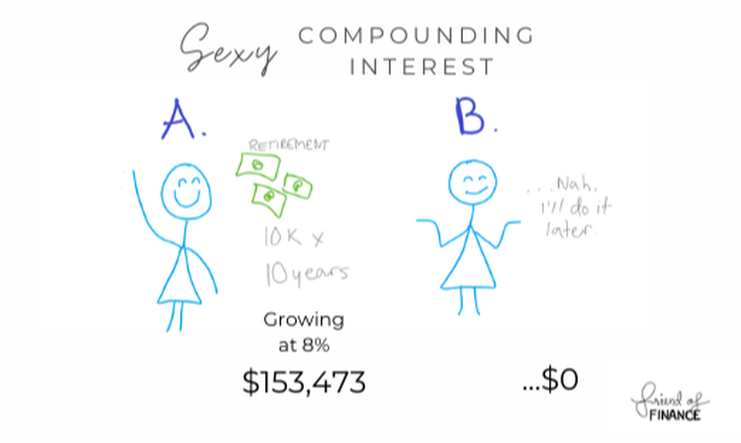

So, you see some tax savings today. But what does your diligent saving get you further down the road? Opportunities for sexy, sexy compounding interest, that’s what.

Pretend Person A starts contributing 10k every year to retirement, and Person B does not. After 10 years, how much does Person A have?

Well, $10k x 10 years would make $100k, right?

Yes... but inside your retirement account you will be invested. How much your account grows each year is not guaranteed, and some years will be negative. But, when you add up all of the years and average them out, you can expect 7-12%, depending on market conditions and the length of time invested. I like using 8%. So 10 years of saving $10k later, Person A has...

Already made over $50,000 from compounding interest! Person B on the other hand... still hasn't started saving.

The longer you are able to invest, the more time you have for compounding interest to work its magic. More time = more magic = more money = more fun things for your future. How does your retirement account grow?

Your retirement account is more than just a savings account for cash, it has the ability to be invested in things like stocks, ETF’s, mutual funds, bonds, and other various investments. If this is where your head starters to spin, don’t let it overwhelm you, this stuff doesn’t have to be complicated, I promise. When we’re investing in equities (stocks, ETF’s, mutual funds... basically anything that isn’t a bond) we are investing our money into companies. Buying a stock is investing directly into said company, where investing in an ETF or mutual fund means you are investing in many companies, probably categorized by index, size, or industry.

Example- You could buy one share of each and every large company that’s traded on the S&P 500 Index (Google, Amazon, Facebook, FedEx, Target, Twitter, Walmart…) or you could buy shares of an index fund that tracks the S&P, and get a small piece of ALL the companies within a single share. If you buy an S&P Index fund (Like Vanguard’s 500 mutual fund, VFINX, or the ETF version, VOO) you are still buying ‘shares’ of the equity, but one share will represent every company currently being traded on the S&P. You will have a smaller piece of each company, but you get a huge amount of diversification all from just one share. When you are a stockholder of a company (or of all of the companies in the U.S stock market) when the companies increase in value, so do your shares. This is why you can get 6%, 9%, 22%, 39%, or even more annual growth on your investments. When the economy is good, and the companies you have invested in are flourishing, your account balance will reflect that. It's important to also be aware and prepared for downturns in the market. Market corrections and bear markets are a completely normal part of investing, but a smart investor should know these can last up to years (cue recessions and depressions) and times where you can see -3%, -12%, -45%... but for the most part, the market is on an upward trend. This is especially true the further you zoom out. This means that the longer you are able to be invested, the better your chances are for long-term growth. So, sexy saves money. Check. Sexy grows money, check. Sexy makes money… How do your retirement accounts make money?

While you could look at your annual growth from your investments and certainly count that as “making money”, there’s even more to be made!

Let me introduce you to dividends. Certain stocks, ETF’s and mutual funds will pay dividends, which are essentially an extra payment that is distributed to stockholders and shareholders, normally made each quarter. While dividends are never guaranteed, many companies have a great long-term history of distributing regular dividends. How large of a dividend you receive will depend on how many shares you own, so the more you have invested, the more your dividends will add up. When you’re in the saving phase, you can also set up to have any dividends you earn automatically reinvested into the fund it came from. When you’re in the spending phase (retirement) you can choose to keep your dividends in cash, and even have them mailed as a check to your front door if you so desire. Some people make enough off their dividends to live off, not even needing to dip into their actual investments for income. Here’s an example of some sweet divs coming into my account. You can typically find this information under ‘TRANSACTION HISTORY’ or some variation of that. See every time it says ‘ORDINARY DIVIDEND’? That was a quarterly dividend being deposited into my account, and then the ‘Bought…@ …’ shows it automatically being reinvested for me. It might not seem like much, but that’s an extra $65.24 that got deposited into my retirement account, that I didn’t put there. And that happens each quarter. And as I continue investing, that number will continue to grow…

I hope you’re starting to see the snowball effect that can come from investing, and how much greater the opportunity is with the more time you have!

Sexy makes money...CHECK. When you have a long time frame for investing, like- 40 years long- it makes saving for such a huge goal SO much more attainable! The sooner you start, the sooner your snowball starts rolling into a big snowball. That means you have the potential for a GIANT SNOWBALL when you retire! But, if you wait until you’re in your 40’s to start thinking about investing for retirement, you would have to save and invest until you are in your 80’s for as big of a snowball. Most people can’t work into their 80’s, so they end up living off of a much smaller snowball instead. Having a smaller snowball often means a lifetime of worrying about whether it’s enough. I’m sure we can all agree on one thing… worrying about money is not sexy. Especially when it’s in the phase in your life where you are getting older, and have been working for the last four or five decades. The sooner you start saving for your future, the less you’ll have to stress about having enough once it’s time to start thinking about retirement. I hope you enjoyed this week’s post! To get updated with new content and get tips on retirement and investing, join the Friend of Finance family below!

2 Comments

Christine

7/16/2020 01:55:09 pm

I love the way you break things down and simplify the financial terms. Thank you for putting this out there and trying to help others!

Alicia Friend of Finance

7/17/2020 09:53:16 am

Thank you for the kind comment, Christine! I'm here to help in any way I can! Leave a Reply. |

Archives

April 2021

Categories |

RSS Feed

RSS Feed