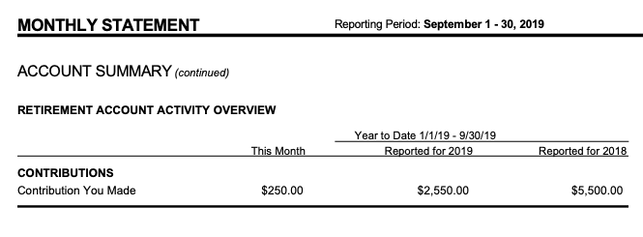

Taxes are a stressful topic for most, but to make tax time a little easier this year check out the top three mistakes made on tax returns- and how you can avoid them!Taxes. Did you wrinkle your nose at that word? Get a shiver down your spine? For most people, taxes are a serious pain point in their adult lives. For the sake of life-long learning, and expanding the advice available on Friend of Finance, I’m currently enrolled in an Income Tax Course, and one-third of the way to becoming an Enrolled Agent (a tax advisor who is allowed to represent people on tax matters before the IRS). What does that mean? That I’m learning a heck of a lot about taxes. And unlike other areas I’ve studied (cough, insurance, cough) the more I learn about taxes, the better I feel. Our system in the U.S can be frustrating at times, but these weird, tricky little math rules that taxes are, are actually set up to help us in a lot of ways, not to try and hurt us. How our tax money is used is a completely different topic that I’m not getting into, but the system behind the Internal Revenue Service collecting our money is constantly evolving because people are trying to improve it. There are a TON of rules when it comes to taxes. But, a lot of these rules are there to protect taxpayers, give credits and deductions to people who need them, and try to make our system as efficient as possible. With that being said, it’s easy to make mistakes and get stressed come tax time. In my last class, I asked my instructor what her top 3 mistakes she saw in her years of experience preparing returns, and to be honest, I was a little surprised with her answers! TAX MISTAKE #1: People claiming dependents incorrectlyClaiming dependents on your return normally points to some kind of deduction or credit (you might remember your parents complaining that first year they couldn’t claim you, and their refund was way less, or nonexistent…) so it’s easy to see why people might try and claim dependents that might not actually qualify. To ensure you aren't getting yourself into trouble, it's important to know who can claim as a dependent and What qualifies as a dependent?A dependent is either a qualifying child or a qualifying relative that the taxpayer provides the majority of support for. There is a difference between the two, which enable different credits. To be a qualifying child, the dependent must be under age 19, or under age 24 if a full-time student. If a dependent is permanently and totally disabled, there is no age limit. They must also have a direct relationship with the taxpayer (child, stepchild, sibling, adopted child, eligible foster child, or direct descendent- i.e. grandchild of any of the above). Qualifying children must live with a taxpayer for over half the year in order to be claimed, and they cannot provide more than half of their own support. If the dependent in question is married and files a joint return for any reason other than getting a refund, they are also not eligible for the qualifying child status. A qualifying relative test is less stringent and gives a few less potential credits than a qualifying child would. Unlike the qualifying child tests, there is no age limit for qualifying relatives, but they must have a direct relationship to the taxpayer (almost all lineages except cousins, but aunts or uncles would qualify) OR a member of the household- defined as someone who has lived with the taxpayer for the entire year. A qualifying relative also cannot have income that is over $4150 (as of 2019) and the taxpayer must provide more than half of the support. If you are claiming a qualifying child or relative, you should be able to prove your financial support to the individual. It’s much easier to prove your support for your own children (birth certificates and school records should do the trick for showing you live in the same household) but things can get more complicated as your potential dependents get more extended. Being aware of what the IRS will look for is a step in the right direction to making sure you are claiming dependents correctly. If you are claiming dependents, you should be able to prove your relationship to them, or that they lived in your home for the entire year if they are not related. You should also be able to prove the financial support you provided to them, and that their own support and income was under the qualifying threshold. Please note, this is a summary- not a fully comprehensive document on claiming dependents! This area is tricky, so if you have questions, please, ask a tax professional. TAX MISTAKE #2: Businesses and self-employed people that don’t keep accurate recordsFiling your taxes when you’re self-employed or a business owner is a whole different ball game. You are eligible for a lot of write-offs that come from your business expenses... but just because you are eligible doesn’t mean you are entitled to them. You need to keep accurate records to prove your expenses, and that they were for your business- not your personal life. A common write-off is mileage, and as of 2019, you get a whopping 58 cents per mile, which can really add up if you are traveling a lot for your business. To claim your mileage though, you should be keeping accurate records. This is not just “X miles on X date”, if you were to get audited the IRS will want to see where you went, how it was related to your business, who you met with, and how far it was. Keeping detailed records as you go is the best way to maintain accuracy, and even if you don’t have to submit your mileage tracker with your return, you need to keep records on file. The IRS is busy, and they can go back several years when auditing. Just because this year’s tax-time has passed and your return has been processed, you aren’t guaranteed in the clear. If the IRS decides they want to audit you for mileage claimed in 2017, they expect you to have a record on file. Keep your records up to date, and do not get rid of them once the year is over! Not providing your records could result in a penalty, nobody wants that. Having accurate records goes for all of your business expenses, not just mileage. Save your receipts for business purchases you are deducting, keep records of all of your income, and treat your personal filing system as if you are going to be audited every year. Staying on top of your business records will make filing your returns much smoother, and it’s worth the few extra minutes a week to organize. TAX MISTAKE #3: Not tracking contributions to a Roth IRAThis is the one I found surprising! Well, not surprising that people are not doing it, but that it made it into the top 3 of my instructor's list. If you know me in real life or are familiar with Friend of Finance, you know how much I love the Roth IRA. The Roth works differently from all other IRA’s, because instead of writing off your contributions in the year they are made (lowering your tax liability) Roth IRA contributions are made with after-tax dollars. This means you are not reporting your Roth contributions when you file your tax returns, and that the IRS doesn’t have a record of your contributions like they would for other IRA’s. If you don’t geek out about investing, you might not be keeping track of how much you have put into your Roth IRA. Since the money in Traditional IRA’s (and 401ks, 403bs, SEP, SIMPLE’s etc.) has not been taxed yet, you will have to pay tax when you pull that money out. But, since the money in a Roth has already been taxed (because you didn’t write it off on the year you contributed, remember?) you can pull that money out tax-free. Now, here’s where the mistakes come in. All IRA’s are designated for retirement, and there is a rule that you cannot pull out your money before age 59 ½ without facing a 10% penalty. This rule is slightly more flexible with the Roth, because you already paid tax on your contributions, you are allowed to pull out the amount you have made in contributions, tax, and penalty-free. But, in order to avoid the 10% penalty, you can only pull out your Roth CONTRIBUTIONS, not your earnings. This is why you need to know how much you actually put into your Roth before you go and pull any out. Let’s look at an example. Say you put $10,000 dollars into a Roth IRA over the course of a few years in your 20’s. You are now in your 30’s, and the balance in your Roth IRA has grown to $18,000, from all of those years of market gains and sweet, sweet compounding interest. You face an emergency, and decide to pull out $15,000 from your Roth IRA, thinking it is tax-free and penalty-free… WRONG! To avoid the penalty, you can pull out only the $10,000 you contributed. Since you took out $15,000, that $5,000 will be subject to the 10% penalty. (Also, please, please, avoid withdrawing money from your IRA's before retirement if at all possible. The money in there is for your future, and pulling it out early means less time for compounding interest working in your favor! You should have an established emergency fund to cover the unexpected, not rely on your retirement accounts)! Disclosing all of your income and its sources is one of the first things you do when filing a return, so when you tell your tax preparer “I took $15,000 out of my Roth, but it’s okay - it’s tax-free!” you should be able to prove that you made $15,000 worth of contributions, to ensure you don’t owe the 10% penalty. The easiest way to track your contributions is by looking at your statement, which should show you how much you have contributed year to date, and the year prior. It's good practice to keep an end-of-year statement in your file with all of your other tax documents for the year, even if you don't plan on taking any withdrawals. Contributions on Statement Example  The majority of these common mistakes boil down to keeping accurate records.

And I’ll be honest with you, if I weren’t actively studying and trying to learn all of these rules, I certainly wouldn’t know them. But as a taxpayer, it’s important to educate yourself on the rules for filing. When you are self-employed, it's even more important. If you don’t want to educate yourself, it’s best to pay a preparer to help you file, to make sure you are following these rules. Takeaways:

Again, I know the topic of taxes is a pain point for many, so if you have questions please feel free to contact me, and I will do the best I can to help. If you have a complex situation, it is worth having a tax professional guide you through it, and this post is not meant to replace the advice of a professional-it was written to give you some insight and thinking points before it’s time to file your taxes. If you want to learn more about the Roth IRA, check out this post. If you want to get serious about a Roth IRA, or other IRA’s, you can schedule a free phone call with me here to discuss your options for opening, funding, and investing within it! Disclaimer: this article is not intended to provide tax advice, please consult with a qualified professional prior to making any tax related decisions.

0 Comments

Leave a Reply. |

Archives

April 2021

Categories |

RSS Feed

RSS Feed