Investing in a SEP IRA or Solo 401k is a great way for entrepreneurs to save money for their futures while saving on taxes today

Being self-employed means you have a lot of stuff on your plate, including planning your investment strategy for retirement. While this might sound overwhelming and difficult, don’t let your fear of the unknown put off your future planning any longer- because it’s not nearly as painful as it sounds.

There are various ways to save for retirement on your own, i.e. outside of an account that’s set up by an employer (like 401k’s and 403b’s) and the two biggies for people who are self-employed are SEP IRA’s and Solo 401k’s. So, what are the differences, and what’s best for you?

Self-employed? Don't forget to grab a free download of this Financial Cheat Sheet! It's full of the stuff you need to know, for your business, and if you print it out and laminate it, also makes a pretty sophisticated coaster for your coffee.

SEP IRA vs. Solo 401k

We’ll start with an overview of the SEP IRA- a surprisingly easy account to manage, especially if you’re a solopreneur.

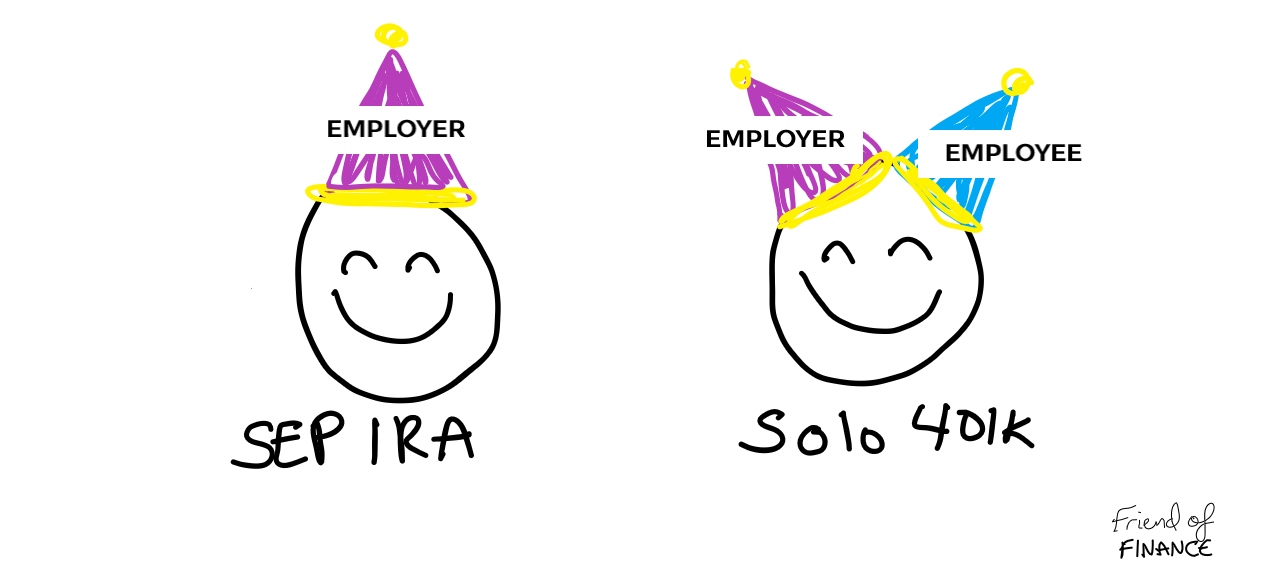

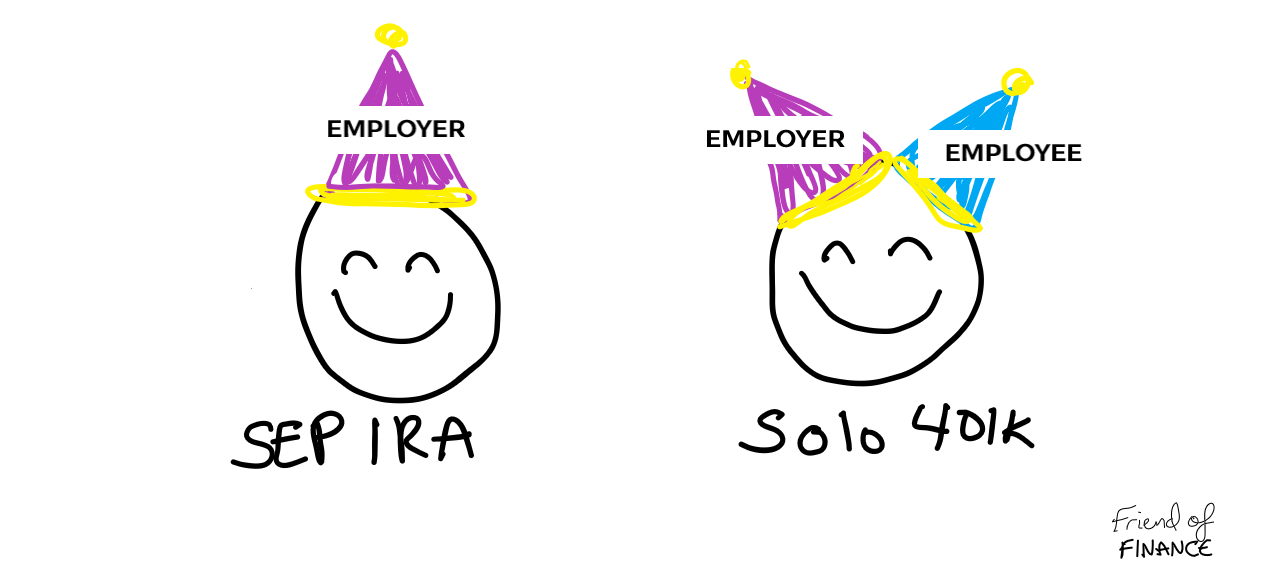

Easy? But it sounds like a mouthful of financial word vomit and I have no idea what those letters even stand for! Yeah fam, easy. And the letters hardly matter- they stand for Simplified Employee Pension, and IRA stands for Individual Retirement Account, but memorizing that isn’t even necessary. I actually like to pretend SEP stands for “Self-Employed Party” because it’s an account you can only open when you’re self-employed, and all those sweet retirement savings are something definitely worth celebrating. A Solo 401k is also worth celebrating, and you even get to wear two party hats! One of the main differences between a SEP and Solo 401k, is with the Solo 401k you are able to make contributions as both the employee, and the employer, whereas a SEP IRA you are only contributing as the employer. We will dig more into these details later.

SEP IRA’s have been around for a while, where Solo 401k’s are a little more new to the entrepreneur playing field. They both have the same objective of being a safe place for self-employed people to save for their futures, but they have slightly different rules and structures. While SEP IRA’s are easier to set up and maintain initially, Solo 401k’s aren’t as difficult to utilize today as they once were.

Both of these accounts come with great tax benefits, like all of your contributions being tax-deductible for the year in which they are made, and both the SEP IRA and Solo 401k will also get the advantage of tax-deferred growth. Taxes are paid only when money is taken out, and both are subject to the additional 10% penalty if funds are taken before age 59.5. You are able to invest your funds inside both the SEP and Solo, so you have the opportunity to grow your money while you wait for retirement. These are all perks that truly compound in the long run, and ones that you will want to take advantage of when you’re self-employed!

But, how do you figure out which one you want to set up for yourself?

The first question you need to ask yourself when you’re considering these accounts is… Do you have employees?

If you have employees, you are not eligible for the Solo 401k, unless your only employee is your spouse. If that’s the case, you both are eligible for individual Solo 401k’s.

If you have employees, you are eligible for the SEP IRA, but you should be aware of the rules. You must contribute the same percentage (not the same dollar amount) for all of your eligible employees as you do for your own account. For example, let’s say Annie has a business and also has two eligible employees, Billie and Casey. If Annie decides she wants to open a SEP IRA for herself and contribute 25% of her earned income into it to catch up on retirement savings, she must also open SEP IRA’s for Billie and Casey, and contribute 25% of their incomes into it as well. We can see how SEP’s can get expensive pretty quick if you have employees. Another catch to the SEP IRA is only the employer can contribute to them, not the employees. If you’re a solopreneur, this isn’t really a problem. But if you have employees, note that you, the employer, will be the only one contributing to these accounts, your employees cannot. There are annual contribution limits for SEP IRA’s, which is up to 25% of earned income, with a maximum of $56,000 for 2019 and $57,000 for 2020. If you want to utilize a SEP you can put as much or as little in as you want, up to those thresholds. If you have employees, the percentage must be the same across the board. Going back to our example, Annie might be thinking “Oh shoot, contributing 25% of everyone’s income is a bit steep. I’m going to contribute 5% instead”. If you don’t have employees, contributing to a SEP for yourself is a lot easier. If you only have independent contractors or freelancers, those don’t count as an eligible employee, so no worries there. The IRS also defines an eligible employee in regards to SEP contributions as someone who has worked for you for at least 3 of the 5 previous years, so if you haven’t had employees for that long, there’s possibly a loophole for you there. Check here to see what constitutes as an eligible employee is in the eyes of the IRS. Other points to note if you have employees, contributing is not mandatory every year, nor is the percentage fixed. All contributions (for yourself and any employees) are tax-deductible for the year they are made. Next question, how much are you making, and how much can you contribute to your retirement?

There are other retirement accounts out there besides the SEP IRA and Solo 401k, and for someone who is just starting out their investment journey, a Tradtitional IRA or Roth IRA is a good place to begin. These accounts can be opened by any individual with earned income, and are easier to open and maintain- but they have a smaller annual contribution limit. For 2019 and 2020 the maximum is $6,000 or $7,000 if you are over age 50. If you don’t see yourself being able to put away more than $6k or $7k, respectively, then I would suggest you start with one of these accounts before opening a SEP or Solo. To learn more about the differences between the Traditional and Roth IRA, I got you covered here.

If you are self-employed and want to put away more than $6,000 (or $7,000 if over 50) then you will want to consider the SEP IRA or Solo 401k. Both the SEP and the Solo have the same maximum limits of $56,000 for 2019 and $57,000 for 2020 if you are under age 50, but if you are over age 50, only the Solo 401k has the additional “catch up” amount. If you are over 50 you can contribute an additional $6,000 for 2019, for a toal of $62,000, and an additional $6,500 for 2020, for a total of $63,500. How you contribute is also slightly different when you are considering these accounts. SEP IRA’s are only funded by the employer, and contributions are calculated as a percentage of income. So if you are under 50 and hoping to max out your SEP in 2020 with $57,000, the only way you are going to get there is if your earned income is $228,000 or higher. Solo 401k’s contributions, however, are made up of both employee and employer contribution. As an employee of your own business, you are allowed to contribute $19,000 for 2019 and $19,500 for 2020 (plus the catch-up if you’re over 50, which is an additional $6,000 for 2019 and $6,500 for 2020). As the employer of your business, you can contribute up to 20% of earned income, or 25% of compensation.

Comparing this to the SEP, you can see that if saving as much as you can for retirement is your objective, then a Solo 401k will give you more wiggle room for making that happen, especially if you’re over age 50 and can utilize the additional catch-up amounts that aren’t available in the SEP. The contributions that you make as an employee are not dependent on your compensation or earned income, so if you have a year where you are making less than normal, or even nothing, you are still able to contribute. Whereas in the SEP IRA, you are always going to be contributing as a percentage of your earned income for that year.

In order to figure out which one is best, you are probably going to have to sit down (preferably with a tax professional) and crunch some numbers for your specific situation. Now, what about the opening process and paperwork?

This is where I prefer SEP IRA’s, as they are easier to open and maintain than Solo 401k’s. You can open a SEP IRA online with most custodians (TD Ameritrade, Charles Schwab, Fidelity, Vanguard…) and it will probably take you less than 15 minutes. The only other additional form you’ll need is IRS Form 5305-SEP (link) and you don’t even need to send this in to anyone, you just need to maintain it in your files.

Solo 401k’s have a bit more paperwork involved, but I honestly can’t tell you firsthand as I haven’t opened one myself. You can still open one with all of the major custodians listed above, but I would recommend talking through the process with a representative at the other end. It’s also important to note that once your Solo 401k has a balance of $250k or more, you are required to file annually with the IRS. If you plan on opening and funding a Solo 401k, it’s important to note that you must open it before the last day of the year, December 31st, in order to fund it for that year. Once your Solo 401k is opened however, you have until Tax Day (normally April 15th, but for 2020 Tax Day is July 15th because of the coronavirus pandemic) to make contributions for the prior year. In our current scenario, we have a rare extension for taxes, and Tax Day has been extended by three months to July 15th. This means that savers are still able to contribute to retirement accounts for 2019. But, if you are self-employed and don’t have any retirement accounts opened yet, and are hoping to still contribute for 2019, the door on opening and funding the Solo 401k is closed for 2019. If you were to open a Solo 401k today, you would only be able to make contributions for 2020. If you already had a Solo 401k opened in 2019 or earlier, you may make contributions for 2019 up until July 15th, 2020. SEP IRA’s have the same deadline for opening and funding- Tax Day. This means there is still a window for self-employed individuals to open and fund SEP IRA’s for 2019. However, you don’t wan’t to leave opening to the last minute, as it can take a few days, or weeks, to finish the process and get online access to your accounts. Still unsure? Remember, you are not confined to one account for the duration of you life or working career. I like to think of retirement accounts as an evolutionary process, and having an idea of how they all work will better equip you for deciding now, and knowing when to use a different account in the future. A few years ago I set a goal to max out my Roth IRA every year. When I became self-employed, I opened a SEP IRA and contribute a modest annual amount- not even close to the 25% of the earned income max, while still maxing out my Roth IRA. These decisions I base on the current tax brackets I’m in (link roth vs trad. blog), which are lower while I’m in my 20’s and still getting my business going. As my business and income grows, so will my SEP contributions. Higher contributions into my SEP IRA will mean lower taxable income in those years. Once I am at a point where I am phased out of Roth contributions, I will be putting more into my SEP IRA, or running the numbers to see if it is more worthwhile to open and fund a Solo 401k instead. Many people get overwhelmed by these accounts, but it’s important to remember that they are here as tools for you and your future- not something to be intimidated by! If you want to learn more about how these accounts work and how you can get set up with them, sign up for my webinar below! (Yes, it’s free).

2 Comments

5/28/2020 12:41:19 pm

Thank you so much for this breakdown! I've been trying to figure out where to stash my side hustle money and this helps!

Alicia Friend of Finance

5/29/2020 09:56:31 am

Awesome, Brittney! Glad this helps! Leave a Reply. |

Archives

April 2021

Categories |

RSS Feed

RSS Feed