Is throwing money at your business really the best move for your future?

Don’t worry, I’m not trying to take you to emotional Ouch-Town, and I’m not taking a jab at people who choose to invest in themselves, their businesses, or their happiness. Not. At. All. All of those investments are crucial for growth, and if we aren’t here on this beautiful planet to grow, what are we doing?

But it’s time to face the truth; some of your investing should also be in stocks. (Or low-cost index funds, of course).

The common question: “What are you investing in?”

The common answers: “Myself!” “My business!” Keep those. Again, those are great things to be investing in, but make sure you aren’t in the group of people that sees spending money on themselves or their immediate needs as an excuse to not invest in other important things, like your future. My financial training came from working at an advisory firm that focused on retirement and helping people figure out the financial aspect to retiring. Don’t confuse this with being biased towards retirement planning and investing- learning (and becoming a little obsessed with) retirement in my 20’s was an eye-opener. I learned firsthand that this process is not one to be taken lightly and that the more money you retire with, the better off you are. I know that seems like common sense. More money = more freedom. More freedom = more time to spend doing the things that make you happy. The part of the equation that most people take too long to learn and act on is the TIME portion. When should saving for retirement start?

Planning and saving for your retirement shouldn’t start at age 60, 50, or even 40. It should start with your very first paycheck. I know most of us are past that point, so if you haven’t started saving for your future yet, the next best time to start is now.

Remember, retirement is a time in your life that WILL come. We are getting closer to retiring every single day, whether we think about it or not. Even if you love your job and want to work for the rest of your life, there will be a time where you are old, and you just might not want to do it anymore. Or, there might be a time where your body simply doesn’t let you. Wouldn’t it be nice to have a nice chunk of retirement savings for when that time comes? OF COURSE, IT WOULD! Or perhaps you are stuck in a grind, and want EARLY retirement to be in your future! I am all for it, and a huge advocate of the FIRE (Financial Independence, Retire Early) movement… but that means SAVING and INVESTING for it! Here’s a closer look at why time is so crucial to your future dollars. 40 Years of Investing

Let’s say 20-year-old Tina starts investing $300 a month in her retirement account and keeps this up until age 60. In my experience with retirees, age 55 is when people start really feeling the burnout from their careers, and mark 60 as their hopeful early retirement age. This might not seem all that early to you, since 67 now marks the official retirement age (at least that’s when Social Security won’t reduce your benefits, if you were born after 1960), but when you’ve been working for decades, every year (shoot, every Monday) you can retire early makes a difference.

Over the 40 years, Tina saved a total of $144,000. Impressive! Enough to retire on? Nope. But, because she was investing in the market with her money and earning an average of 8%*, her money was growing and compounding. Her account value is now over $1,000,000 with over $910,000 coming from compounding interest! Almost a million from market gains and compounding growth! Say whaaaat?!

*Market performance is NOT guaranteed! I use 8% when estimating for retirement, but you can explore with different returns. The average of the Total U.S Stock market averaged 11.9% in annual returns over the last 10-year period and just under 8% since 2001. Past performance does not guarantee future results!

Minus the fancy planning and specific calculations, Tina looks to be in decent shape for retirement, not to mention is a self-made millionaire!

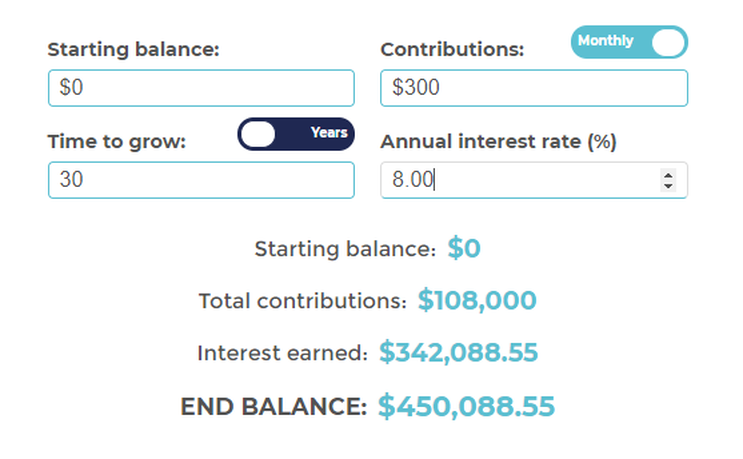

30 Years of Investing

Now let’s see what 30-year-old Thea’s situation looks like. She also saves and invests $300 a month, but is starting at age 30, and hopes to also retire at age 60.

Over the 30 years, Thea contributed $108,000 to her retirement account, only $36,000 less than Tina. But her end result? $450k. Less than half of Tina’s ending balance! In order for Thea to reach a million dollars at her current savings rate, she would be working and saving until age 70.

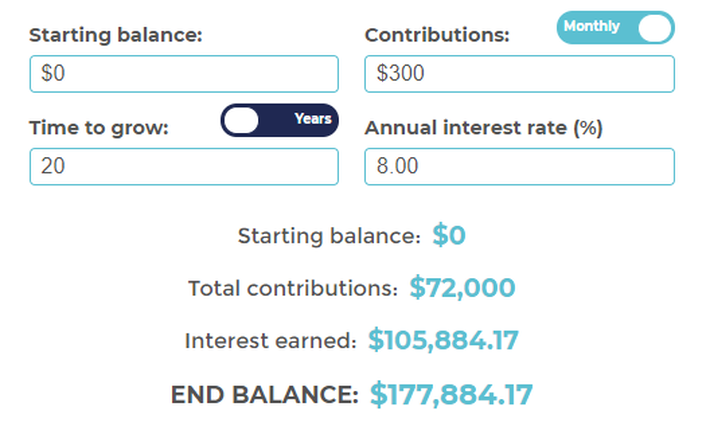

20 Years of Investing

And what about 40-year old Fiona? Again, same numbers, except we subtracted another 10 years from the “Time to grow” section, giving Fiona a 20-year investing horizon.

Fiona contributed $72,000 over the 20 years, and earned $105,884 in interest, leaving her with $177,884. While it’s awesome that her gains from the market and compounding surpassed her actual investment, she is far away from millionaire status. At this savings rate, 20 more years away, meaning Fiona will have to work and save until age 80 in order to retire a millionaire.

When people are close to retirement age and facing numbers like this, they have a few options.

It’s the harsh reality, but it’s the truth. If you aren’t investing for your future yet, you probably didn’t realize how valuable your time really is! I encourage you to run your own numbers, you can find my calculator (the same one in the pictures) here. Play with some realistic numbers, and then with some crazy ones. Give yourself an average growth of 5%, 8%, and 12% to explore the realm of possibility. Play with investing $50 a month and then $5,000. See how early you can retire, or how long you could possibly be working. Time is an ingredient that we can’t get back, so if you are feeling on the wrong end of this example, try not to focus on the time you don’t have. Focus on the areas you CAN control; how much you invest (which might mean taking steps to increase your income) and making the decision to invest. Because you aren’t going to see an 8% return on the money sitting in your checking account! If you are feeling overwhelmed by this and want to talk about it, you can schedule a 20-minute Discovery Call with me here- for free. What’s your answer going to be next time someone asks "So, whatcha investing in these days?” I hope it includes “my retirement accounts”!

Hey, are you part of the Friend of Finance family yet? If not, sign up below to hear when blogs come out, and get all of the sweet financial nothings whispered straight into your inbox.

1 Comment

christine Zittel

9/17/2020 08:06:36 am

"Retire with what they have, depend on Social Security and government assistance, and stress about money for the rest of their life" Lol! You left out "depend on your intelligent, wealthy children to help you out" I love you. I am so so proud of you. xxxxxxxxx000000000000 Leave a Reply. |

Archives

April 2021

Categories |

RSS Feed

RSS Feed