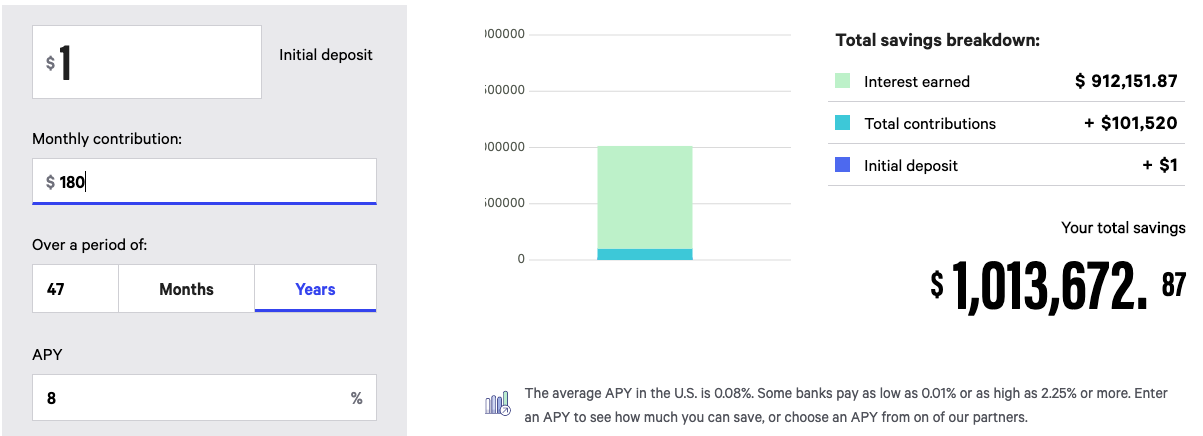

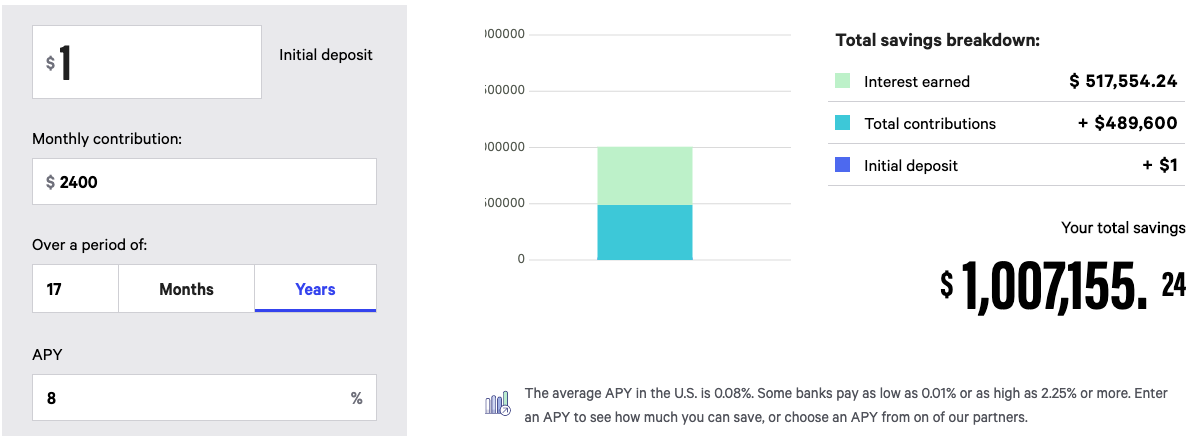

Financial goals that you can achieve in 20 minutes or less that will have you feeling good for the rest of the year.The start of a new year is always exciting, full of rejuvenation, goal-setting, and what feels like an opportunity for big changes that are much-needed in your chaotic life… ...and then the champagne wears off, and January 1st starts with a hangover instead of a gym session. Or you might have found yourself in the mindset of being completely over failed resolutions, that you didn’t even bother setting any goals for yourself this year. And hey, that’s okay. But, just because we are into the second week of January doesn’t mean you can’t make some small adjustments to your life that can set this decade up for success. Nobody is perfect, and creating longstanding habits is hard. The trick is to implement small, easy tweaks that will stick, not giant, life-changing goals. Another goal-setting tip is to avoid vague resolutions that won’t really get you anywhere. Instead of “I’m going to be better with my money in 2020” or “I’m going to save more”, try resolutions that are specific and actionable, and ones that will help you throughout the year with little to no ongoing effort. The following three goals are just that- things that are easy to implement yet will leave you feeling good about yourself all year long. 1. Switch Your Savings AccountEstimated time to complete: 10 minutes Cost: $0 Reward: an additional 1-2% in interest on your savings, maybe more in the future. Earning more on your existing savings is possibly one of the easiest ways you can save more this year, and it's an easy switch to make. For example, if you have an emergency fund with $10,000 earning 0.01% over the next year, it will look like $10,001 by the time you’re making next year’s resolutions. Not much to be excited about here. But, taking 10 minutes to open a new high yield savings account where you can earn a higher interest (rates will vary based on the fed’s interest rates, but as I write this there are places offering around 1.7-2% APY) your $10,000 will look more like $10,180 if earning 1.8%. Worth it? Uh, yeah. Not only will you instantly feel good about making this smart money move, but you really don’t have to do much after the initial set up to continue reaping the rewards. 10 years from now you are looking at a difference that’s in the thousands, and that’s if you don’t put in any additional money or effort. I'm not affiliated with either, but two high-yield savers I have tried are Synchrony and Ally, with Synchrony offering a slightly higher rate, and Ally being a little more user-friendly. Either way, both will give you more than that minuscule fraction of a percent you're getting now. 2. Automate Your SavingsEstimated time to complete: Less than 5 minutes Cost: $0 Reward: That’s up to you. I’ve personally found that I save up to 4x as much when I automate it, versus trying to save money the old fashioned way… aka, seeing what’s left in my account before I get paid next. Automating your savings is an essential- and something that I was recently reminded of just how important it actually is. A few months ago, I turned off the automatic deposit I had going into my (high-yield, of course) savings account. My reasoning at the time was I was focusing my efforts on saving for something else, and I would just be better about limiting my spending and transferring what was available over, rather than my scheduled amount. Guess what happened? Without my money being taken from me before I could spend it...I spent it. Whoops. Looking back on the last four months of saving, I realized that I saved a lot less than I could have. When it comes to socking money away for yourself, 9 times out of 10, you are your own worst enemy. Figure out how much you can reasonably save each month or each paycheck, and set up that amount to go into savings as soon as the money is available in your checking account. Take advantage of automation, and get your hard-earned cash out of your dangerous, spendy-pants hands. 3. Do Something About RetirementEstimated time to complete: 20 minutes + time spent procrastinating Cost: $0 Reward: The weight off your shoulders of carrying this adult thing you should have figured out already, but haven’t. The money you save for your future. The compounding interest you’ll get over your upcoming years in the market. To see what this looks like in $, check this out. Now, I realize I told you not to set vague goals, and then contradicted myself by listing the super vague goal “Do something about retirement”, but bear with me for a moment, and I will give you something more actionable that’s based on where you are currently in your retirement journey. The younger you are, the more excited you should be about retirement. Wait, whaaa? Seriously. If you are in your 20’s, now is the perfect time to be thinking about retirement. My daily life revolves around other people’s retirement, and one of the biggest problems I see with younger generations is they have no idea of how big of a goal retirement actually is. Retirement is normally associated with age, but just because you turn 59.5 and can now access your retirement accounts, doesn’t mean you’ll have enough in there to retire. Especially if you aren’t saving for it now. If you plan on waiting until your Social Security benefits kick in, a.) I hope they’re still there for you and b.) I hope you understand that living solely off government programs probably won’t provide the quality of life you want. Once you realize that the more money you have saved for retirement the better your life will be, the sooner you can actually start this rewarding process. Keep in mind, your goal with retirement savings is to someday replace your income. How long will it take you to save up one year of income, if you’re currently saving 3%? Not accounting for interest or market growth, 33.3 years. And how long will it take you to spend it? One. And people are living longer than ever before, meaning we have longer, and more expensive retirements to fund. Luckily, this is where the magic of investing, compounding interest, time, and employer contributions can all have a huge impact on your retirement savings, and understanding and utilizing these tools will better set you up for the future. The sooner you start saving for retirement, the more time you have for your money to grow. A nice looking account, one that has six or seven figures, is made up of two very crucial things. Money. And Time. You only need a lot of one of them, so you can either try to save a lot of money over a little time, or you can put away a little money, over a long period of time. Assuming both examples below are investing in retirement accounts and earning an average of 8% a year; if an 18-year-old saves $180 a month until they are 65 (47 years) they will end up with a whopping $1,013,672. The most exciting part about this? That sea-foam green rectangle of “Interest earned: $912,151.87”. The MAJORITY of this balance is from interest, aka, from time spent in the market.  But if you wait until you’re 48 to start saving, in order to hit $1 million by age 65 you’ll need to save $2400 a month. While the interest earned is still impressive, it’s not nearly as profound as it is in the above scenario. And if you’re a person that has struggled to save your entire life, it’s likely that it will not be any easier for you the closer you get to retirement.  The exact numbers aren’t what I’m trying to get across, the point is- the sooner you start, the easier it is.

If you like playing with savings calculators though, this is what I used for the examples above: Bankrate's Simple Savings Calculator. Seeing the impact of what your current savings can do for future you is a great way to get hyped about retirement if you’re not already. Now, the actionable options for this resolution: 3a. If you are offered an employer plan like a 401k, 403b or 457 through your work and you are not currently enrolled- ENROLL. This means going out of your way and talking to your boss or HR person, and filling out the necessary paperwork. It’s likely this is something you’ve probably been putting off for a while, years even, but remind yourself “NEW YEAR, NEW ME!”, and go do it. 3b. If you don’t have access to an employer plan, check out this post on how to save for retirement without one. It involves some initial setup, and probably some more motivational mantras about being the best version of you that you can possibly be, but it’s not difficult, I swear. (And if it is too difficult, contact me here, and I’ll do it for you). 3c. If you have a 401k or 403b set up already, increase your contributions this year (unless you are already maxing your account). Even a small increase of 1% will have a great impact on your bottom line come retirement time. 3d. If you have a Traditional, Roth, or SEP IRA you are contributing to but not maxing out, set a goal to increase those contributions. It could be an extra $10 a month, or an extra $100, just make sure it’s something you can set and forget for the rest of the year. And ta-dah! A few minutes on your computer looking at your accounts and a couple of small tasks for set up, and your financial goals can be on autopilot for 2020. Because let’s face it, the less hands-on you have to be, the better. Now we can take all this free time that used to be spent worrying about money and spend it at the gym, right? To learn more about working with me as your advisor, feel free to schedule a complimentary call with me here. I'm that person that will listen to you cry about your spending problems, and then help you fix them.

1 Comment

|

Archives

April 2021

Categories |

RSS Feed

RSS Feed