This wealthy-feeling milestone might not stretch as far as you think...

A millionaire. $1,000,000. What is it about this number that makes it so significant? The 6 zeros? The TWO commas? Or is it simply the first financial milestone that actually has a title? (Hundred-thousandaire just didn't catch on or what?).

Even though being a millionaire or winning a million dollars seems like a lot of money, inflation, the result of a slowly but ever-increasing cost of living, needs to be considered. The more time that passes...the less one million dollars actually is.

That can be a problem for millennials and younger generations. If you remember that movie from the '90’s, Blank Check, (where a kid runs into a convict and somehow manages to get a blank check which results in a backpack full of one million dollars cash) then the idea that “one million dollars can buy you literally anything in the world!” might be living in the depths of your mind still. When actually, this huge-sounding financial milestone may actually be a necessity to live a comfortable life by the time the millennial generation retires. The problem(s) for future generations and retirement...

-Most of us aren’t thinking about it, which means we aren’t actively saving for it.

-We have other expensive crap to pay for, like student loan debt, homes, cars, weddings, kids, virtual reality headsets, and pet insurance because- just kidding, we actually can’t afford to have kids! So we end up justifying our reasons for not saving, instead of saving. -Things previous generations have been able to rely on for income, like pensions and a fully-funded Social Security system, either aren’t around, or are not a guarantee. What does that mean? That retirement is going to be more expensive, we are saving less for it, and that we will be getting less from employers and cannot guarantee on getting as much assistance from the government. Oof. Hey, when is this party going to lighten up? I thought you said there would be drinks here… The good news. We do have one thing older generations do not when it comes to this retirement game. Time. The sooner you understand investing and how to use the stock market and retirement accounts to your advantage, the easier this expensive goal is. The key is learning, and acting. Let’s get to the numbers. First, how much will you actually need in retirement?

Most people don’t really stop and think about what retirement actually is until they are right around the corner from this phase. Retiring means you’re no longer working for a traditional paycheck, and you instead get your income from other sources, like pensions, Social Security, and your own personal savings- things like 401k’s, 403b’s and IRA’s. These are all investment accounts that are designed specifically for retirement savings and have nice tax perks too. But if you don’t know how much you will need when you get to retirement, how do you know how much to save today? Or over the course of your working life?

A million bucks. Will it be enough? This isn’t a yes or no answer, and it will obviously be very dependent on your lifestyle. If you’re used to spending $100k+ a year, have a huge mortgage, and a lot of debt, and you want a million-dollar retirement account to fund a 25-year retirement, the answer is a big fat NOPE. Where if you’re a frugal person living in a tiny house on a piece of property that is paid off, you could probably make a million dollars last a few retirements. (Or retire early). To know what will be enough for you, I’ll take you through the well-used financial rules of thumb, the rule of 25, and the 4% rule. Keep in mind, these do not replace actual financial planning when retirement approaches- but they are handy for a little guidance to those that are in the saving phase. The rule of 25

This is used to give guidance on the “How much should I have saved?” question. Having an ending amount can help plan what monthly or annual savings should be, to make sure you hit your target on time (or at least come as close as possible).

According to the rule of 25, you take the amount of income you want in retirement and multiply it by 25. That amount should be what your retirement savings equal upon retirement. If you want to take out 100k of your investments every year, you should have $2.5 million saved by the time you retire. 100,000 x 25 = 2,500,000 So, according to this rule, if you have $1 million, you can withdraw $40,000 annually. 40,000 x 25 = $1,000,000 If that’s all you want or need in retirement, then congratulations, $1,000,000 will be enough! Wow, a millionaire and all you get to live off is $40k a year? Keep in mind, if you have been paying into the Social Security system, the idea is there will be some retirement income coming from that source too. The current monthly average benefit is $1503, however, Social Security is currently expected to only be fully funded until 2034 and then 79% funded after. Sooo, there's that. The 4% rule

This is another rule that coincides with the rule of 25, stating that you can withdraw 4% of your investment accounts every year and not fear running out of money. This is because your invested money is still growing and compounding, and by you only taking out what you need, as you need it, the rest is left to grow. As long as you don’t take out too much, your growth will offset your withdrawals, leaving you with income for the rest of your life. Multiplying our target income by 25 is one way to use the 4% rule, but if you skipped that part and want to know how much you can take out of your accounts at their current balance, just multiply your total balance by 4%.

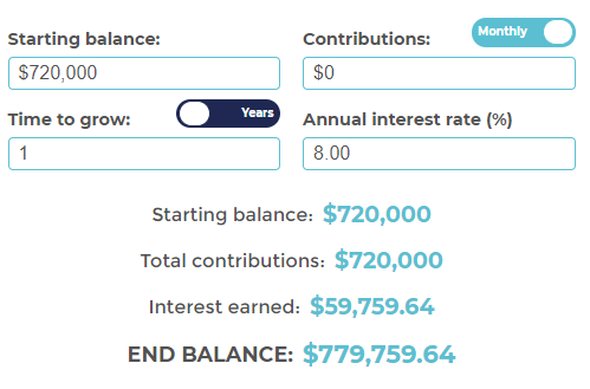

Say you have $750,000 invested. $750,00 x .04 = $30,000 According to the 4% rule, you could safely take out $30,000 annually. Year 1: $750,000 - $30,000 = $720,000 If your investments grow by 8% that year, your account has magically replenished, plus some. $720,000 x 8% = $779,759.64

The problem is, we have no idea how much our investments will grow, or in which direction. Some years will grow a lot, and others will lose money. All we know is that over a long enough period of time, we will average out in the upward direction.

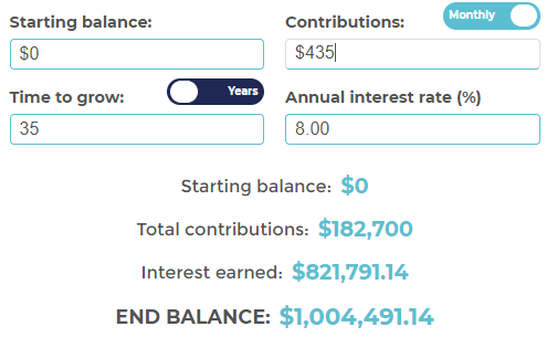

Again, these are “rules of thumb”, not necessarily formulas you should be basing your entire future around, especially as the future unfolds and you get closer to retirement. We really have no idea what the markets will do over the next 10, 20, or 30 year period, and all investing comes with risk. But these tools are enough to at least get you on the right track and help guide your savings goals. And what about inflation? If millennials range from age 22 to 38, we’ll use 30-year-old Thea for our example. Thea is 30 right now, and saves $435 a month for her retirement. 35 years from now she wakes up on her 65th birthday. Today is the day. It’s time to retire. And the best part? She’s a millionaire. Her investments in her retirement accounts finally moved into that 7th digit. $1,004,491.14. She couldn’t be more proud.

The year is 2055. If inflation increases at 2.5% per year, how much purchasing power does $1,000,000 have in today’s dollars?

An inflation calculator will show that in 2055, you would actually need $2,373,205.19 to have the same purchasing power as $1,000,000 in 2020. So 30-year old Thea who is now 65 years old? Her $1,000,000 has the purchasing power of $421,371.07. Whhaaat?! But that's less than half! I know. Inflation can be brutal AF. Wow, Alicia, you’re really taking the wind out of my sails here… and where are those drinks you were talking about? Don’t get me wrong, saving a million dollars is still a great goal, and is certainly a lot of money. We just need to be careful and not let our brains think it’s more than it actually is, and honestly answer the question on an individual basis. Will it be enough? I know, the further you go down the rabbit hole of planning for the future, the more daunting it can seem. That’s why it’s important to be aware of this now because when you are investing, time is your most valuable tool. If you want to continue this conversation over virtual drinks, you can book me for a free call here. If you want to play with some numbers, and see how much your savings can grow if it’s invested, or figure out how much you should be saving to retire a millionaire (or a 2.5 millionnaire) head over to my compounding calculator. And if you aren’t a member of the Friend of Finance family yet, get your name in that little box below!

0 Comments

Leave a Reply. |

Archives

April 2021

Categories |

RSS Feed

RSS Feed