There's a good chance millennials are under-prepared for retirement, especially those who are self-employed.

It’s easy to categorize retirement in the “I’ll figure that out later” column, especially for millennials who have a good thirty to forty years before reaching the traditional retirement age. In fact, it is a lot easier finding reasons to NOT save for retirement as a millennial, whether it’s having a mountain of student loan debt, saving for a down payment on a home, other life expenses like weddings and starting families, or simply that investing is a complicated and maybe intimidating subject area. Since most retirement saving that DOES happen is done through employer plans like 401k’s or 403b’s, millennials who are self-employed are probably even less likely to be saving for retirement.

Self-employed? Make sure to grab a free copy of this Financial Cheat Sheet, your business will thank you.

As a self-employed millennial who used to be a financial advisor, the topic of retirement for my generation is one of the things that keeps me up at night.

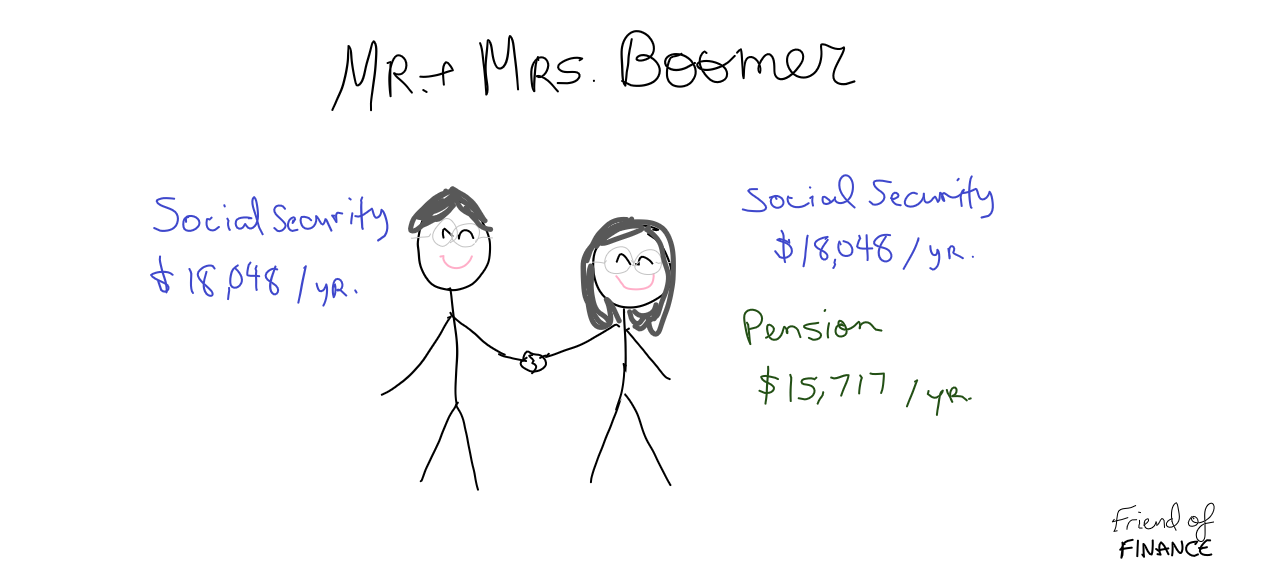

Retirement is something that the majority of people don’t really understand the complexities of until they are a few years away from it. I know this, because I spent three years working with people who were fast-approaching retirement, and all of a sudden the mentality shifts to “Oh wow, I plan on retiring next year… how do I actually make that happen? Do I have enough money to leave my job now, or do I have to wait five more years?” The strategy of “crossing that bridge when we come to it” is risky for all generations, but works better for the generation that’s retiring today, baby boomers. This is because there are a few more resources available to today’s retirees to generate income. But can the millennial generation afford to avoid retirement planning until the last moment? I really don’t think so, and here’s why. Each generation that passes through retirement has different hurdles. The baby boomer generation retiring today might feel stressed out with Social Security and pensions, and figuring out how much they need from their personal investments to bridge the income gap that might exist from those sources. But millennials… are likely to be responsible for their entire income in retirement, not just bridging the gap. From my experience, many retirees today have three sources of retirement income, pensions, Social Security, and personal savings (401k’s/403b’s, IRA’s, investment accounts and savings). While not everyone has a pension, they are certainly a lot more common for the boomer generation than the ones following. Let’s pretend a couple retiring today wants to live off of $50k a year. The average Social Security Benefit in 2020 is $1504 a month, or $18,048 annually. The median pension range is $9,262 for private pensions, and $22,172 for federal pensions. If we use an average between the two for the sake of keeping the math simple, we have $15,717. If we say a couple retiring today has Social Security benefits for each individual, and one person has an average pension ($18,048 + $18,048 + $15,717) they would have $51,813 in annual income, without even dipping into their investments. They’re goal of $50k of retirement income has been met!

If the couple was hoping for a more expensive lifestyle, yes, more would need to be taken from their investments. So lets say they want to live off $75k a year, meaning they need to take $23,187 a year from their personal nest egg. In order to afford that (without fear of running out of money) the nest egg should equal at least $579,675, according to the simple “rule of 25”.

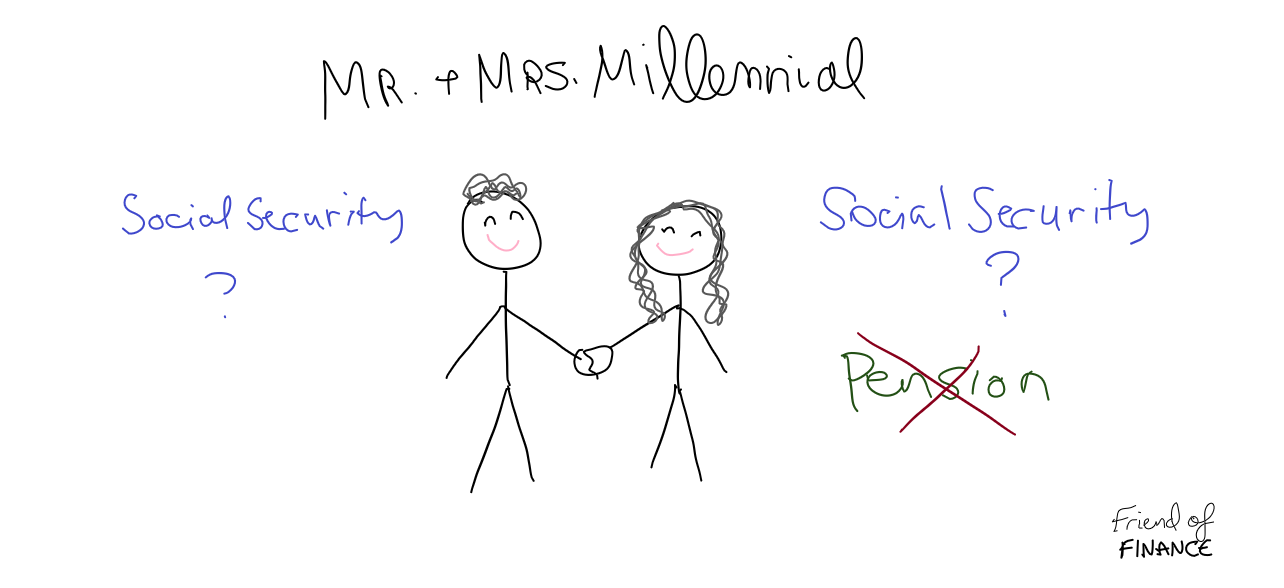

The rule of 25 is used to determine how much you should have invested or in your nest egg when you retire. You take the amount you want to withdraw annually, and multiply it by 25. Easy peasy. Want to withdraw $100k a year? You’ll need a nest egg of $2.5 million. Because this money is invested, it will be growing at a rate that is higher than what you are taking out, creating a self-sustaining flow of money to see you through the rest of your life. Now, let’s compare that to the millennial generation. Can I see a show of hands for those who have a pension? And what about those who have faith in the Social Security system?

While I would love to see Social Security benefits for my generation, I’m not so sure. According to the Social Security website, "Social Security is fully funded until 2034, and after that it is about three-quarters financed". Sounds less than three-quarters promising, if you ask me. The millennial generation will be turning 60 in the 40’s and 50’s, and are probably hoping to retire somewhere in that time frame. How funded will Social Security be then?

If we use our example from earlier, a couple wanting to retire with $75k a year, and with today’s estimates of Social Security, millennials MIGHT be able to expect 75% of today’s Social Security benefits. 75% of today’s average benefit equals $13,536. Pensions are out, so that means a total of $27,072 from each individual’s Social Security benefit, leaving $47,928 to be drawn from personal investments. Again, using the rule of 25, the millennial couple’s nest egg should be $1,198,200. This is twice as much as retirees today, for the same amount of income. So, who wants to tell the millennials that are still paying off tens of thousands of dollars of student loan debt, prolonging buying houses and starting families, that they also need to save over a million dollars in order to have a decent retirement? While this goal seems huge, it is completely achievable if you have time on your side, and if you get an early start on investing for retirement. That means making saving a priority now- not putting it off for future you to figure out. The reason this is especially important to those who are self-employed is that they don’t have the main resource used for saving for retirement, 401k plans through an employer. While there are plenty of alternatives, setting them up takes effort and research, and then consistent discipline to actually make the contributions. When you look at all of the reasons why saving for retirement now is difficult, the majority of people will continue to do just that- not save. But when you pause and consider the alternatives… working until you’re 80, downgrading your lifestyle to live off only Social Security, or moving in with your kids, what’s more painful? Time is half of the equation when it comes to building wealth, and money is, of course, the other half. If you feel like you’re lacking on the money side, then you need, need, NEED to utilize your time! A little money mixed with a lot of time can go a long way when it comes to investing, so if you’re a millennial who hasn’t started investing for your future yet, make sure you aren’t wasting your most precious resource! Financial education is lacking, especially in the realm of retirement and investing. If you don’t know where to get started, check out this post that simplifies investing into 5 easy steps. To stay tuned in and get my updates and investing tips, sign up to join the Friend of Finance Family below!

6 Comments

christine zittel

6/25/2020 09:06:24 pm

Wow! I need to share all your info. This information has to get out to the younger generation. It's not fair that the millennials will be paying for the baby boomers but that's the reality. You, have the knowledge and the passion to help so many millennials achieve the future they deserve and dream about. Never stop sharing and teaching.

Alicia Friend of Finance

7/2/2020 03:22:46 pm

Thank you for your kind words, Christine! We all can do great in the world by teaching and learning, and I don't plan on stopping either any time soon! :)

Alicia Friend of Finance

7/2/2020 03:23:43 pm

I'm glad this post could help you, Mer! Thank you for sharing your favorite line! :) 7/8/2020 10:29:58 am

I have felt these underlying fears about my own retirement. You did a great job of breaking down the technical aspects and giving facts to the underlying fear. Well, I think I am going to see if I can throw some more money at my investments.... 😉

Alicia Friend of Finance

7/17/2020 09:52:11 am

Thank you for sharing your thoughts, and relating in the fears! It's unfortunate that fear and money are so often correlated, but you have the right attitude! The more you can save now, the better! :) Leave a Reply. |

Archives

April 2021

Categories |

RSS Feed

RSS Feed