The extension for 2019 taxes also impacts IRA contributions, which means you could be in an extended “sweet spot” for catching up on savings.

Saving for retirement is a hefty topic, one that many like to put off until it is arguably “too late”. As the saying goes ‘the best time to plant a tree was yesterday. The second best time is today”. This saying applies to saving for retirement perfectly. When I was a financial advisor and working with retirees on a daily basis, one thing was said again and again... “I wish I had known more about investing when I was younger.” Why do so many people say that? Well, once you have had money invested for a while, you truly understand the magic of compounding interest. And what’s compounding interest’s best friend? Time. Time is the reason a saver who starts investing $500 a month from age 20 (and earns an average of 7%) could retire with over $1.2 million. But if they wait until age 30? The ending balance is less than $600k. You need two things to grow wealth, money and time. You only need to have a lot of one of those things.

So far, 2020 has been a wild year for retirement savers. If you aren’t saving yet, you might find this the perfect time to start... 2019 Tax and IRA Contribution Extension because of COVID-19

We are in an unprecedented time as the world tries to manage the coronavirus pandemic. The economy is suffering. At the time of writing, my state is coming up on it’s sixth week of a mandatory shelter in place order, which will go on for at least another three weeks. You are only allowed to go to work if you are an essential worker, while everyone else is experiencing a transition to working from home, or worse- facing furloughs and lay-offs. Unemployment rates are skyrocketing, and the unemployment offices are struggling to get everyone through the systems. When you do leave your home, wearing masks and gloves in public is strongly recommended, along with a 6-foot distance being kept between you and anyone else.

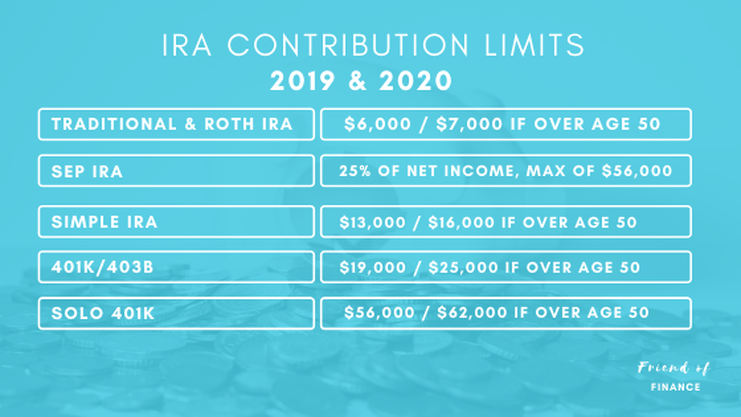

This sci-fi series-esque life we all woke up in last month might be consuming your thoughts. If you have found yourself struggling to make ends meet because of all of these changes, my heart goes out to you. Your current bills, debts, and making sure your families needs are met is always your top financial priority. Only when these needs are met, should you consider investing money for the future. But, if you have found yourself monetarily unaffected by all of this, now might be a great time to catch up on your retirement savings. Most Americans use employer sponsored plans, things like a 401k, 403b or 457 plan, as their main way of saving for retirement. Those that are a little more financially-savvy are also using investment accounts that can be opened and funded by themselves, the most popular being Traditional IRA’s, and Roth IRA’s. People who are self-employed might also be contributing to Solo 401k’s or SEP IRA’s. So, what does the coronavirus have to do with all of this? In a normal year, we have until ‘Tax Day’ (which is normally April 15th) to fund IRAs for the previous year. But with everything going on, we all got an automatic extension for taxes, with a new deadline of July 15th, 2020. New Tax Day? New contribution deadline for IRAs. This means you now have until July 15th 2020 to fully fund your IRA for 2019! This is not an event that occurs often, so if you are in a position where your finances have not been affected by the pandemic, and if you haven’t started saving for retirement or maxed out your contributions for 2019, you are in a rare time that you can take advantage of. Read this if you are confused about investing and don’t know where to start. If you have IRA accounts already opened, and would like to take advantage of the extension for contributions, here's what you need to know. IRA Contribution Limits for 2019 and 2020

The contribution limit gets adjusted every few years, and 2019 and 2020 saw an increase from previous years.

Whether you are allowed to deduct your Tradtional IRA contributions or make Roth IRA contributions will be based on your Modified Adjusted Gross Income, or your MAGI. Your retirement accounts have some sweet tax advantages, which is why you’ll see the taxy stuff associated with them. The more you make, the less you’re allowed to take advantage of these accounts, so check where your AGI is on the tables below before continuing.

Traditional IRA Income Limits for Tax Deduction

If you and your spouse are NOT offered a retirement plan like a 401k or 403b through your employer, these limitations DO NOT apply! You may contribute and deduct the full amount.

If you are contributing to a 401k/403b, you are still allowed to contribute to a traditional IRA, however, if your income goes over a certain threshold, your contributions will not be deductible. AKA- you can't write them off when doing your taxes. Money in Traditional IRA's get's taxed as income when it is pulled out in retirement, so if you aren't getting the tax write off now, your contributions could end up facing double taxation. Single or Head of Household Filers:

Married Filing Jointly or Qualified Widowers:

Income Threshold for Roth IRA Contributions

The big difference between Roth IRA's and Traditional IRA's is when you pay tax. If you are contributing to a Traditional IRA, you deduct your contribution from your income when you file your taxes, therefore, are not paying any taxes on it...yet. When you pull money out of your Traditional IRA, it will be taxed as income. If you pull it out before age 59 1/2 you also risk an additional 10% penalty.

When you contribute to a Roth IRA, you are using after-tax money, and not writing off your contributions in the year you make them. You don't see the tax savings today, but since you already paid taxes on that money, all of your contributions and gains can be pulled out tax-free after age 59 1/2. If you pull out money before that, only the gains will face the 10% penalty. High-earners get phased out of being allowed to contribute to a Roth IRA, see if you are eligible to make contributions based on the tables below. Single and Head of Household Filers

Married Filing Jointly and Qualified Widower Filers

If you’re in the sweet spot for contributing to an IRA, you have until July 15th, 2020 to contribute for 2019, and assuming the world is normal next year, April 15th, 2021 to contribute for 2020.

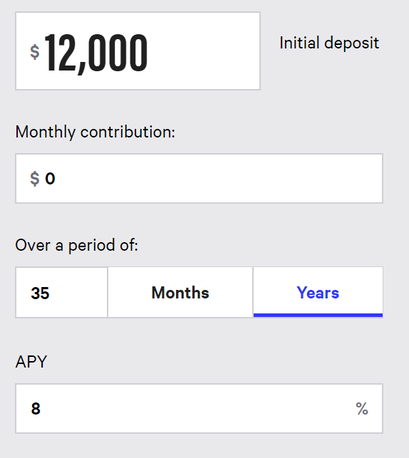

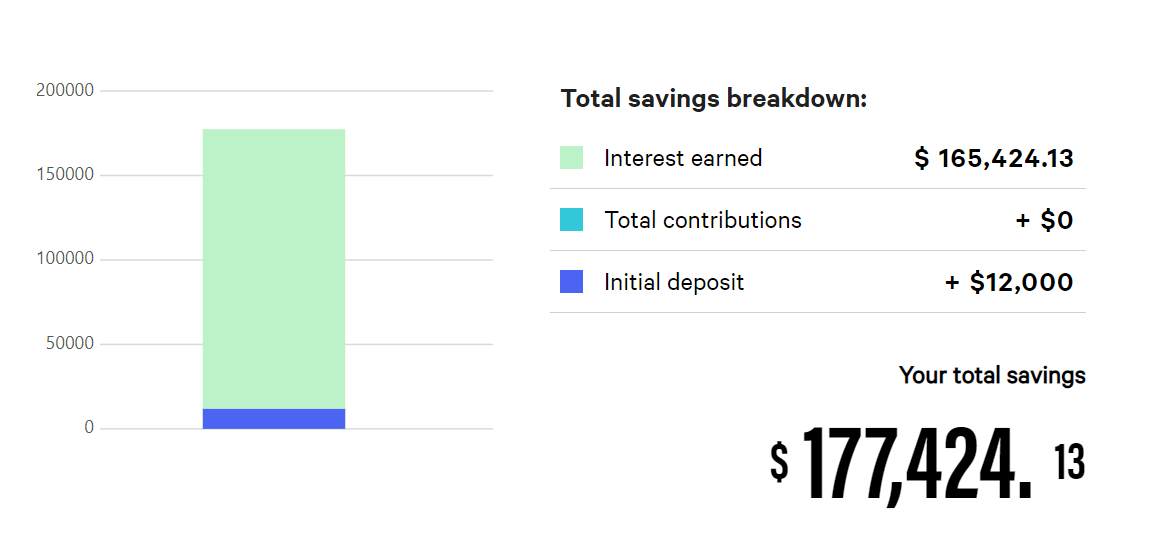

I’m going to paint a picture of an ideal scenario for this time... You are in your 20’s and you haven’t started saving for retirement yet. You finally realize that it’s important, and are excited to start saving immediately! Your paycheck has been unaffected by the pandemic, your emergency fund is healthy, and you just received a bonus check of $15,000… you could open a Roth IRA, put in the full $6,000 for 2019, and another $6,000 to fully contribute for 2020! You could go from feeling behind on your retirement savings, to being fully maxed out for 2 consecutive years! Let’s say you are 25, and you do this, and ONLY this. You put in $12,000 today, and don’t invest ANYTHING else for the rest of your life. If you earn an average of 8% annually, that $12,000 will grow to $177,424. See what I mean about the secret ingredient being TIME?!

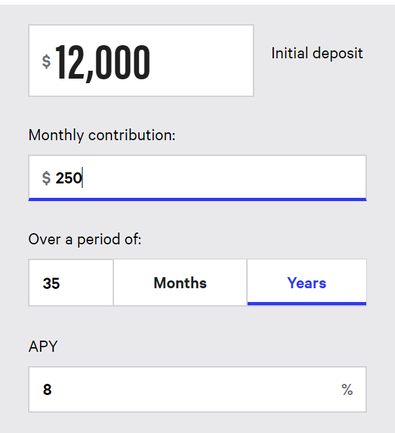

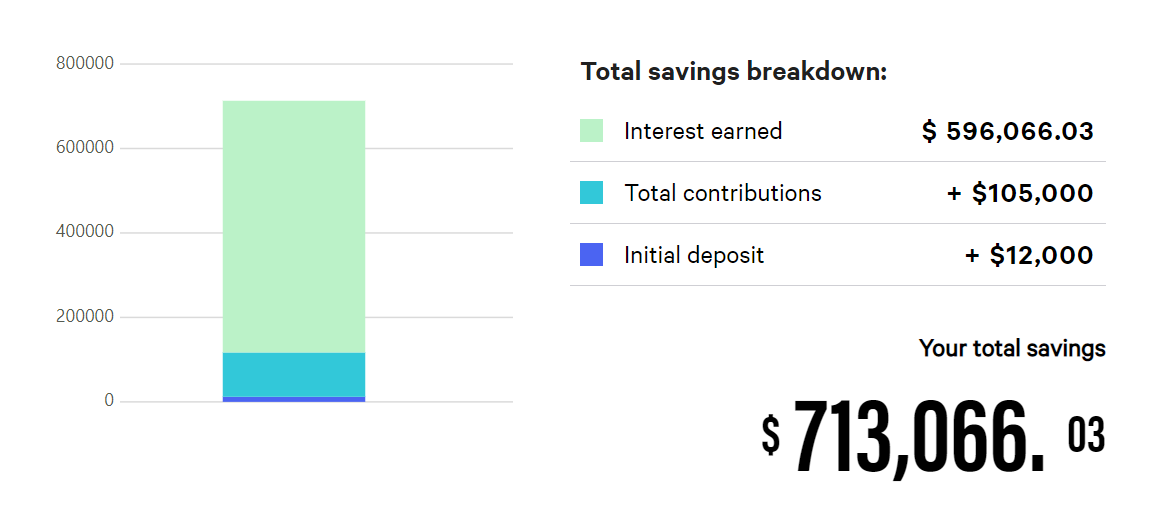

And what if, like most others who start investing, you find that you don’t want to just contribute one time, that you’d rather invest a little every month. Maybe you decide to prioritize your future more, and decide to put $250 into your IRA every month after making the initial $12,000 contribution. After 35 years of earning an average of 8%, your account would be…

$713,066! Your contributions, or the amount you actually put into your account over the years, totals $105,000. That’s certainly an amount to be proud of! But the cool part? You earned almost $600,000 in interest.

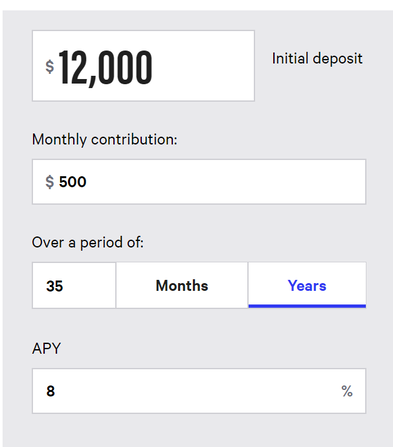

You might be thinking, “well shoot- if I was able to max out my Roth or Traditional IRA for 2019 and 2020, I want to make it a goal to max it out EVERY year!” To that I would say- YES! YOU DEFINITELY SHOULD MAKE THAT YOUR GOAL! To keep it simple, after our initial $12,000, we will increase the monthly contributions to $500, which equals $6,000 a year, the full contribution amount. If you are able to contribute $500 a month and max out your retirement accounts for the next 35 years, you will likely find yourself in the two comma club come retirement time.

(These calculations are made using Bankrate's Simple Savings Calculator, plug in your own figures here!)

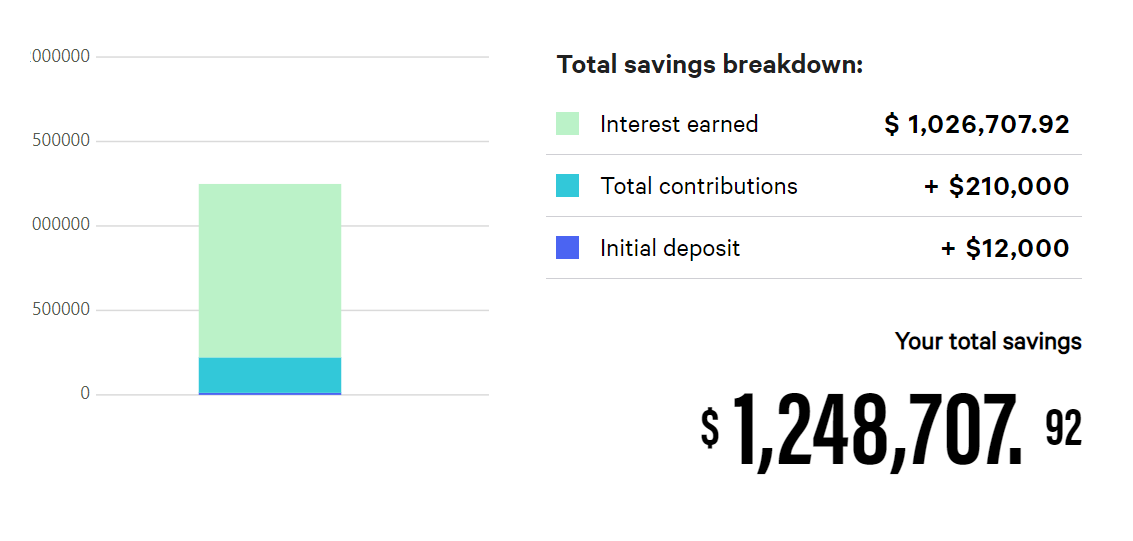

If you earn an average of 8% annually, your IRA would be $1,248,707. Almost 1.25 million dollars, after a total of just $210,000 in contributions. That’s over a million dollars earned in compounding interest. Did you hear that right? Yepp. If it’s that easy, why isn’t everyone doing it? Well, it’s “easy” on paper. Being disciplined enough to put the money away you have today, and telling yourself you can’t have it for decades… not so easy. It’s like that marshmallow experiment, where kids are given a marshmallow that they can eat now, or wait a few minutes and get two. Are you the kid that eats your marshmallow as soon as it hits your sticky palm, or do you wait patiently to earn two marshmallows instead? Your finances are SO important, but sometimes thinking about money... sucks. I get it! I do my best to make it less sucky, to get financial tips and to hear about new posts, join the Friend of Finance community below!

1 Comment

|

Archives

April 2021

Categories |

RSS Feed

RSS Feed