Student loan debt is something a growing number are struggling with. This is my personal experience with managing student loan debt so far.It's a quiet morning, I know the stock market has been slipping the last few days so I pull up the 'Stocks' app that's incorporated into Apple products nowadays, confirm that yes, everything does seem to be down by a percent or two. I click through a few articles, one on the student loan epidemic, another on how president Trump apparently hasn't been playing by the rules while filing his tax returns...

It all makes me sad and angry. When we grow up and become contributing adults to society, the first few years can be intimidating. Taxes are a complicated subject, student loans are arguably even more complicated, along with everything else we must do. Mortgages, probably, but I can't speak from experience on that yet because I'm still renting. There's a lot of red tape, rules to follow, and processes that must be completed in a certain order. Let's look at student loans and the loan forgiveness program. Student loans have been a part of my life since the age of seven, and not because I was a super genius that started college at a young age, but because that's when my mom decided to go back to school, and I became aware of being poor.

1 Comment

Understanding how life insurance works is the first step in making an educated choice for you and your family.Life Insurance, it's not for you-it's for them.

Let's start with the basics, what is life insurance? Similar to other types of insurance you may already have, life insurance is a contract between yourself and an insurance company. As long as your premiums are paid, the insurance company will provide a sum of money (called a death benefit) to your named beneficiaries in the event of your death.  The start of a new year is a great time to reflect on the previous year and establish goals for the year ahead. Since many of our finances are structured on an annual timeline, like yearly contributions to a retirement account, this is a great time to put goals in place.

The more specific your goal, the more likely you are to achieve it, but below are some common financial goals to provide a starting point. Goal: Max out your Retirement Accounts For 2019 the annual contribution for 401(k)’s, 403(b)’s, and most 457 plans have increased to $19,000 (up from $18,500 in 2018) and Traditional and Roth IRA’s have also seen a $500 increase, raising the annual limit to $6,000 (up from $5,500 in 2018) (1). This is great news for those who are already maxing out these accounts, and for those who are trying to catch up before retirement. The more money you can sock away in pre-retirement years, the better these accounts will look when you need them. For those that have maxing out their Traditional IRA or Roth as a goal and were already struggling to hit the limit, don’t let this $500 increase be discouraging. If you can increase your contribution to $6,000, this $500 bump will look great in your account by the time you retire! That extra $500 invested now earning a 7% annual interest turns into over $5,000 in 35 years (2). If you are able to max out your IRA consistently, you are potentially increasing your future balance by tens of thousands.

A lot can happen in 10 years, and as time goes on, it only seems to moves more quickly.

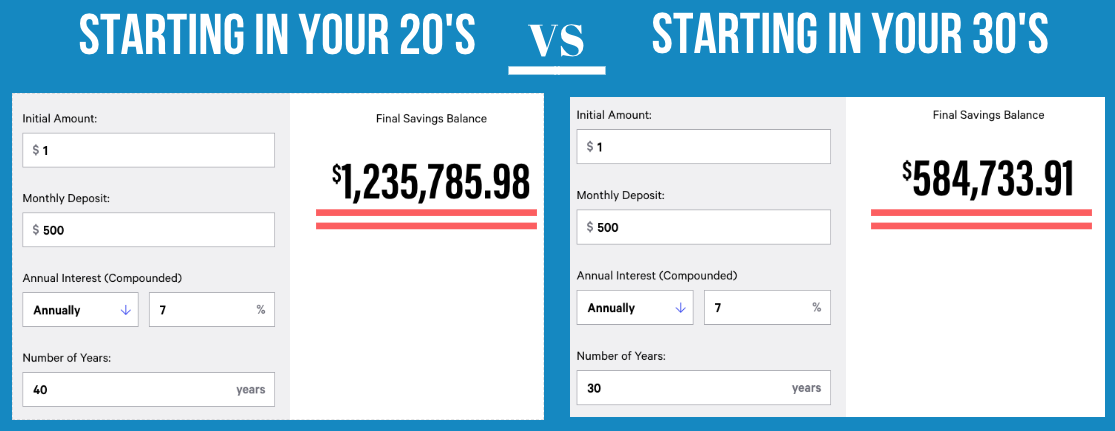

Many things have the gift of growing and flourishing over time. A nice wine, a planted seed, your retirement account. Just like a small seed that will eventually become a great tree, your retirement account has to start somewhere. The sooner you get that seed in the ground, the larger it will be by the time you retire. Most people in their 20’s are not in their peak earning years yet. Paychecks may feel like they are already stretched too thin, and because of this, many put off saving for retirement. You may not have been offered a 401k at work in your lifetime, and maybe you never even thought to start saving on your own. There are always reasons not to save, but the longer you accept these reasons, the less you are giving to your future self. In the two examples below, $500 a month is invested for 40 years and 30 years, earning an annual 7% interest. The ending balance after 40 years is DOUBLE what it is for 30 years. Double. Let that sink in.

Starting a Roth IRA in your 20's is arguably one of the best financial move's you can make for yourself.One of my goals as a financial advisor is to help open up a Roth IRA for everyone I know. Ambitious, I know, but hopefully, that helps show how valuable I think a Roth IRA truly is.

Let’s start with the basics, what even is an IRA and how is a Roth IRA different?  Saving for retirement is something you don't want to procrastinate, because the sooner you start, the greater the potential benefits of compounding interest in your account.As we get older, we understand there are things we should be doing, or should be getting better at, and are vaguely aware of strategies we should be implementing throughout our adulthood. Some of these things have a heavy financial focus, and if they are topics we don’t truly understand or deem them too difficult for the moment, they get pushed onto a to-do list for our future selves.

One of the major tasks many 20 or 30-somethings decide to wait on is planning for retirement. I get it, something that is 40 years away is not at the forefront of your mind when you see this week's paycheck hit your account. You need to focus on this months bills, student loan payments, saving for a down payment on a house, saving for a wedding, paying childcare expenses, paying off your credit card… the list goes on.  Retirement for millennials seems far away, but because of the changing landscape of retirement income, saving should start now.What will retirement look like for the millennial generation? This may seem like a loaded question, and full of unknowns, and that’s because it is. We are looking at three to four decades of time passing before the millennial generation embarks on retirement, during which, a lot of change can happen. Changes to Social Security, Medicare, and cost of living are all inevitable, and changes we won’t be able to predict accurately at this time.

For the sake of this piece, we are going to go on what we know today, and the generation that is currently retiring, the Baby Boomers. |

Archives

April 2021

Categories |

RSS Feed

RSS Feed